11

11

The debate between buying new and buying used is one of the most common questions in personal finance. The honest answer is that it depends on numbers — not emotions, not the smell of a new car interior, and not the appeal of being the first owner.

Compare New vs. Used Car Costs →

This guide walks through the complete financial comparison of buying new versus used, how to calculate the true cost of each, and which choice makes more sense at different income and budget levels.

New cars win the emotional argument almost every time. The latest safety technology. A full manufacturer warranty. No unknown history. Zero previous owners. That fresh-from-the-factory feeling.

Used cars win the financial argument more often than most buyers realize. Lower purchase price. Avoided first-year depreciation. Often just as reliable when purchased from the right source. And in many cases, the “new car” advantages disappear within 2–3 years of the vehicle’s life.

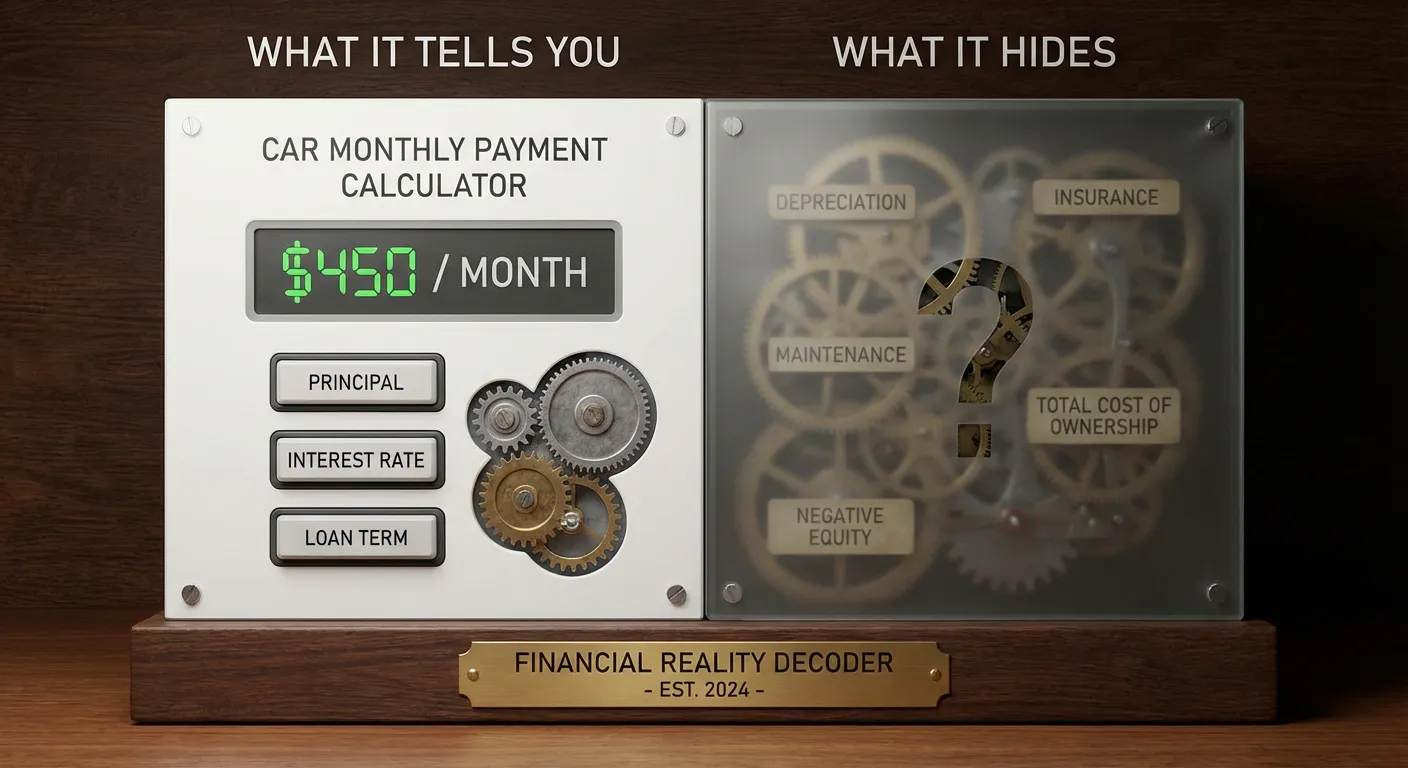

The goal of a good new vs. used car cost calculator is to strip away the emotion and show you what each choice actually costs over the time you own the vehicle.

Depreciation is the largest cost of owning a new car — larger than loan interest, insurance, or fuel for most buyers. Yet it is the cost that almost no one calculates.

Here is how depreciation typically works on a $35,000 new vehicle:

| Year | Depreciation | Remaining Value | Cumulative Lost |

|---|---|---|---|

| Purchase | — | $35,000 | — |

| Year 1 | $7,000 (20%) | $28,000 | $7,000 |

| Year 2 | $4,200 (15%) | $23,800 | $11,200 |

| Year 3 | $3,570 (15%) | $20,230 | $14,770 |

| Year 4 | $3,035 (15%) | $17,195 | $17,805 |

| Year 5 | $2,579 (15%) | $14,616 | $20,384 |

By year five, the car is worth $14,616. You paid $35,000. The depreciation alone cost you $20,384 over five years — that is $4,077 per year purely in lost value, not counting loan interest, insurance, or fuel.

This is why buying a car that is 2–3 years old is often described as “letting someone else take the depreciation hit.” You buy a car that still has most of its useful life ahead of it, at a price that reflects the steepest portion of depreciation having already occurred.

Let’s compare buying the same vehicle new versus buying the same model that is 3 years old with 36,000 miles.

Vehicle: Mid-size sedan

| Factor | New | 3 Years Old / 36k Miles |

|---|---|---|

| Purchase Price | $35,000 | $22,000 |

| Sales Tax (8%) | $2,800 | $1,760 |

| Doc + Registration | $700 | $400 |

| Down Payment | $5,000 | $3,000 |

| Amount Financed | $33,500 | $21,160 |

| APR | 6.5% | 9.0% |

| Loan Term | 60 months | 60 months |

| Monthly Payment | $655 | $439 |

| Total Interest | $5,800 | $5,181 |

| Annual Insurance (est.) | $1,900 | $1,600 |

| Annual Fuel (est.) | $2,200 | $2,200 |

| Annual Maintenance (est.) | $800 | $1,400 |

| Resale Value at Year 5 | $14,600 | $8,000 |

Five-Year Total Cost Calculation:

New car: Total loan payments + interest: $39,300 Insurance (5 years): $9,500 Fuel (5 years): $11,000 Maintenance (5 years): $4,000 Less resale value: -$14,600 Total 5-year cost: $49,200

Used car (bought at year 3): Total loan payments + interest: $31,541 Insurance (5 years): $8,000 Fuel (5 years): $11,000 Maintenance (5 years): $7,000 Less resale value: -$8,000 Total 5-year cost: $49,541

In this comparison, the five-year cost is nearly identical. The new car wins on total cost by a small margin due to lower maintenance and lower APR. The used car wins on monthly cash flow by $216/month — which is significant for a tighter budget.

The used car becomes clearly better value when you extend ownership beyond 5 years (the new car keeps depreciating while loan on the used car is paid off) or when the new car is a high-depreciation model.

Buying new makes more financial sense in these situations:

Manufacturers occasionally offer 0% APR financing on new vehicles. When this is available, new cars become significantly more competitive financially. A $32,000 new car at 0% APR for 60 months costs $32,000 total. The same car at 3 years old at 8.5% APR costs roughly $38,000 total. The new car wins by $6,000.

These deals are typically available on outgoing model years and specific trims — and they require excellent credit (usually 720+).

Some vehicles — particularly from Toyota, Honda, and Mazda — are well-documented as having very low ownership costs over 10+ years. Buying these new and keeping them for 10–12 years spreads the depreciation cost over a long enough period that the per-year cost becomes highly competitive.

If you buy a $30,000 reliable sedan and own it for 12 years, your depreciation cost is roughly $2,500/year. That is quite reasonable.

Advanced driver assistance systems (ADAS) — automatic emergency braking, lane-keeping assist, blind-spot monitoring — have improved dramatically in the last 3–5 years. If safety technology is a priority, buying a car with the latest generation of these systems may warrant the new car premium, particularly for families.

Buying used makes more financial sense in these situations:

When total budget is under $25,000, the used market offers significantly more vehicle per dollar. A 2–3 year old midsize SUV with 25,000–35,000 miles can be purchased for $25,000–$30,000 when new it sold for $38,000–$42,000. The same $25,000 buys a much smaller, less equipped new vehicle.

Some vehicles depreciate extraordinarily fast — luxury brands, electric vehicles (in the current market), and certain American-made full-size trucks. A 2-year-old luxury vehicle that sold for $55,000 new can often be purchased for $35,000–$38,000 used. That is 30–35% price drop in 24 months.

These used vehicles offer exceptional value because the premium content (premium interior, advanced tech, larger engine) is largely intact, while the price has fallen dramatically.

Even when the five-year total cost of new and used is similar, the used car delivers significantly lower monthly payments. For someone managing a tight monthly budget, $216/month in extra cash flow each month is meaningful — it is $2,592 per year that can go toward savings, debt payoff, or emergency fund building.

Certified Pre-Owned programs offer a middle ground between new and used. CPO vehicles are:

CPO vehicles cost 5%–10% more than non-certified used cars of the same model, but the extended warranty and lower APR often make them the best total-value purchase in the market — particularly for buyers who want some protection against unexpected repair costs.

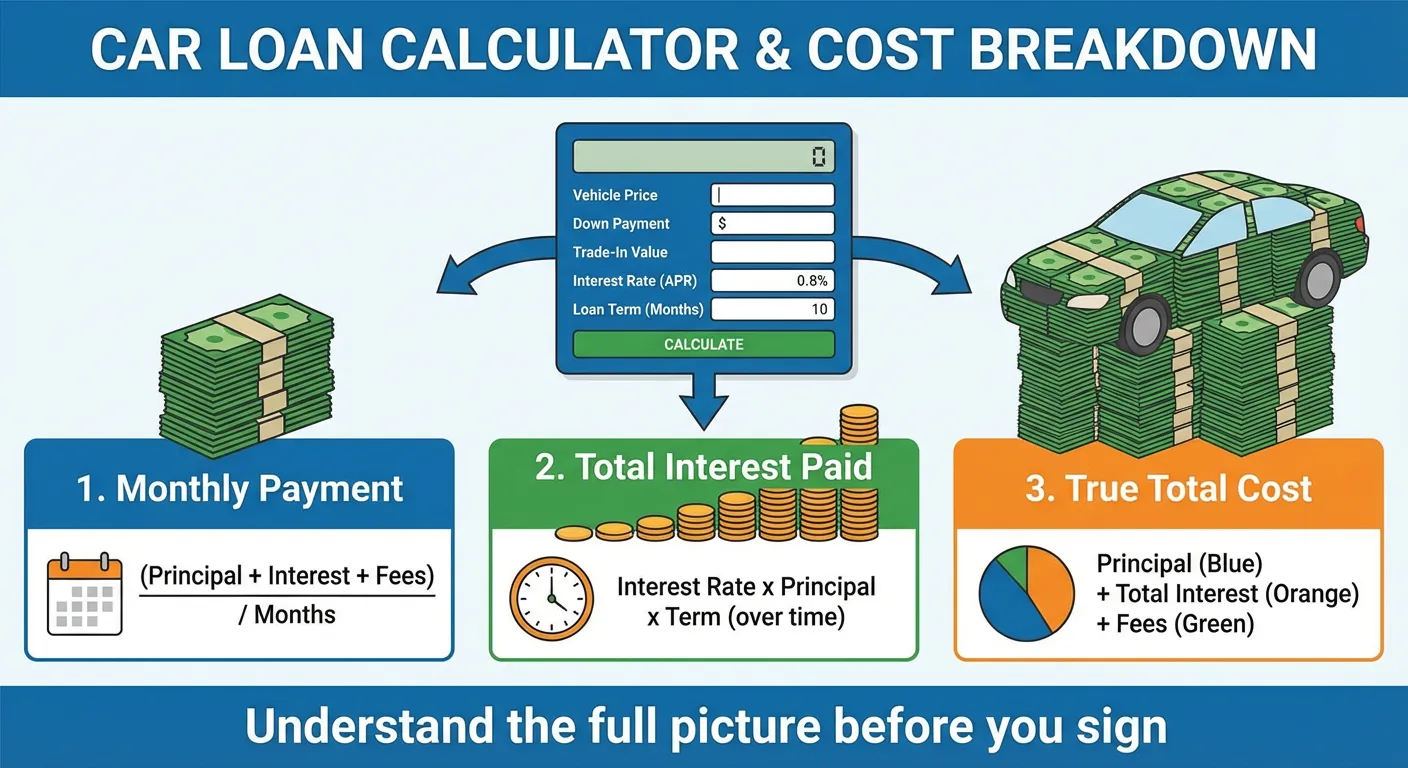

A new car cost calculator should capture every element of the purchase:

Each of these variables changes your out-the-door price and your financed amount. Most buyers focus only on the MSRP and monthly payment. The full calculation — the one a good new car cost calculator provides — includes all twelve variables and shows both the monthly payment and the true total cost of the vehicle.

A used car cost calculator has a few additional variables:

The key additional output of a used car calculator is the depreciation forecast — how much the vehicle is likely to be worth in 3 and 5 years, and therefore what your total cost of ownership will look like versus what it looks like at first glance.

One of the most misunderstood parts of either a new or used car purchase is the trade-in. Here is the clean way to think about it:

Net trade-in equity = Trade-in value – Amount you still owe

If your trade-in is worth $12,000 and you owe $8,000, your net equity is $4,000 — which acts like an additional $4,000 down payment.

If your trade-in is worth $12,000 and you owe $15,000, you have negative equity of -$3,000. This amount gets rolled into your new loan, increasing what you owe from day one. This is called being “upside down” and it is a significant financial risk — you are starting a new loan already owing more than the car will be worth if anything goes wrong.

Dealers often obscure negative equity by presenting it as “we will pay off your loan” — which technically is true, but they roll that balance into your new loan. Always calculate your net trade-in equity before walking into a dealer.

Most car cost comparisons look at 5 years. But if you keep a car for 10 years, the calculation shifts significantly in favor of the new car (for reliable models).

Here is why: the new car’s loan is paid off in year 5. Years 6–10 you drive the car with no loan payment, modest maintenance, and a vehicle that is still reliable. The annual cost in years 6–10 drops to insurance + fuel + maintenance — roughly $4,500–$6,000/year.

The used car buyer who keeps buying used every 4–5 years is always in a loan. They benefit from lower monthly payments, but they rarely experience the “no payment” years that long-term new car owners enjoy.

For buyers who commit to keeping a vehicle long-term, buying new and maintaining it meticulously is a completely valid financial strategy.

| Annual Income | Recommended Strategy |

|---|---|

| Under $40,000 | Used car, 3–7 years old, $8,000–$14,000, paid in full if possible |

| $40,000 – $60,000 | Used car or CPO, 2–5 years old, $14,000–$20,000 |

| $60,000 – $85,000 | CPO or modestly priced new, $20,000–$30,000 |

| $85,000 – $120,000 | New car or recent CPO, $28,000–$42,000 |

| Over $120,000 | New or low-mileage used luxury, up to $55,000 comfortably |

These are guidelines, not rules. Your individual debt situation, family size, commute, and financial priorities all affect the right answer for you.

Use our new and used car calculator to enter your specific scenario and see exactly what each option costs over 1, 3, and 5 years — including the total interest paid, depreciation estimate, and true monthly cost of ownership.

[Compare New vs. Used Car Costs →]