11

11

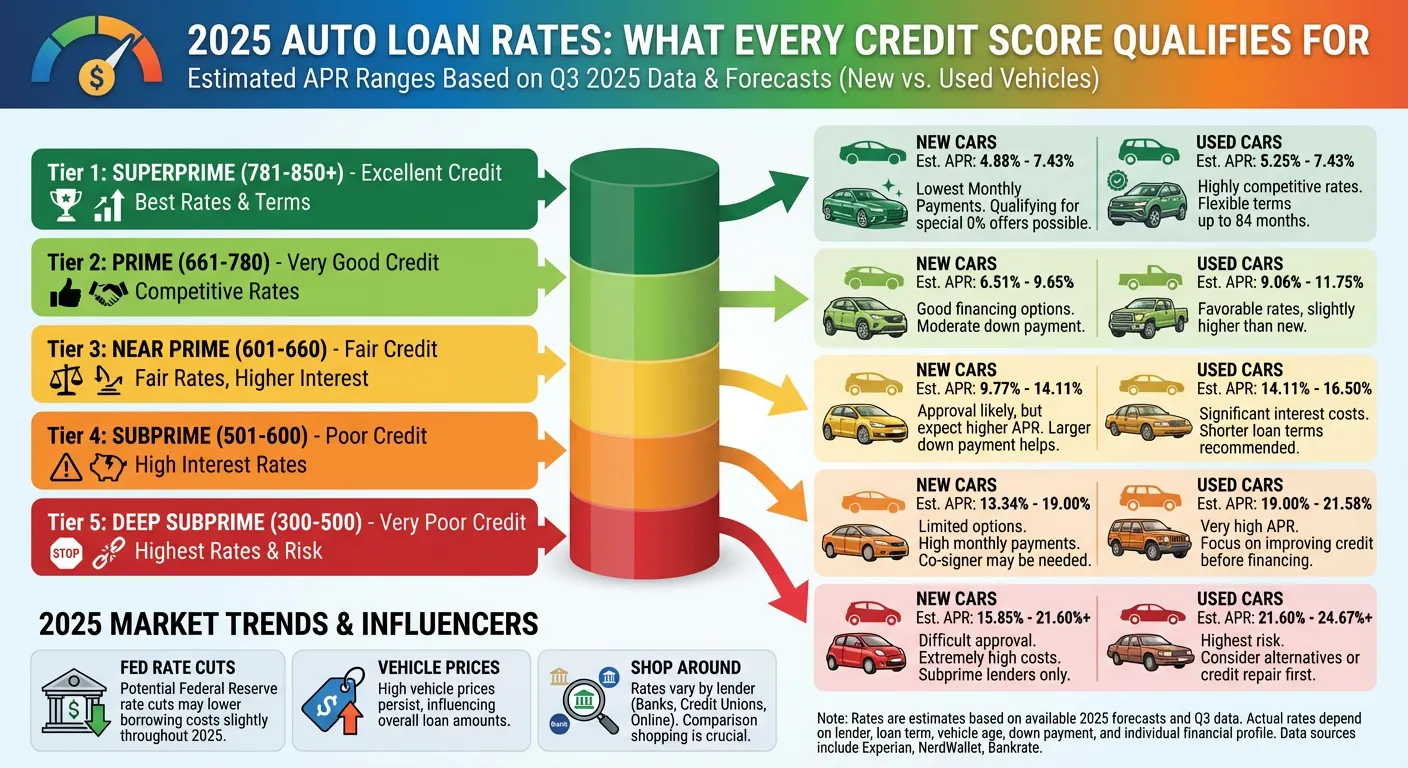

The single question every car buyer wants answered before stepping into a dealership is: what interest rate will I actually get? The answer depends almost entirely on your credit score — and the difference between the best and worst auto loan rates isn’t a few percentage points. It’s the difference between paying $3,000 in interest and paying $15,000+ on the same vehicle over the same loan term.

This complete guide covers current average vehicle financing rates for every credit tier, explains exactly what lenders look at beyond your score, shows you how different rates translate to real monthly payments, and tells you precisely what to do if your score isn’t where you want it to be.

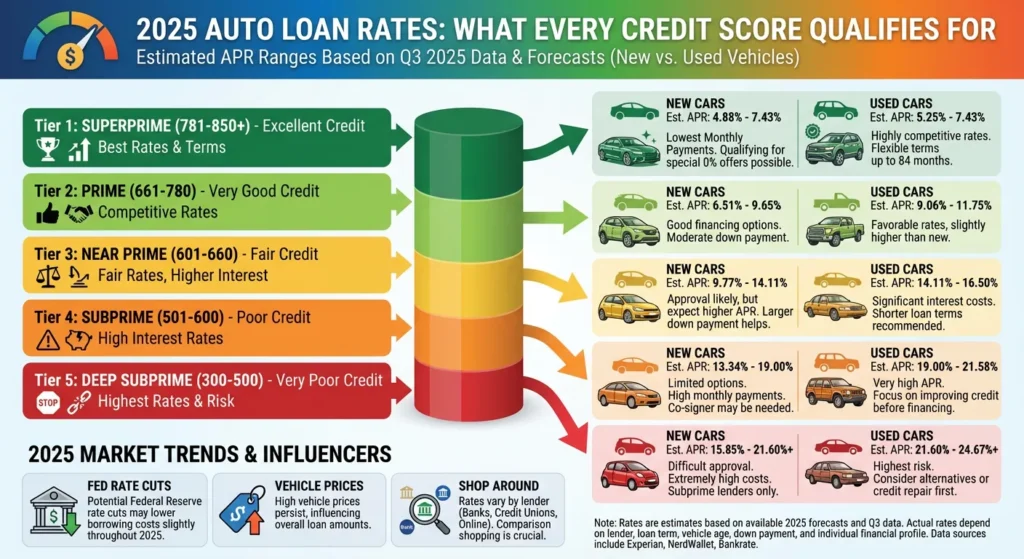

The following rates are based on Experian’s State of the Automotive Finance Market and Federal Reserve consumer credit data. These are averages — your specific rate will vary based on your lender, the vehicle, the loan term, and your complete financial profile.

| Credit Tier | Score Range | Average APR | Monthly Payment ($25K, 60mo) | Total Interest |

|---|---|---|---|---|

| Super Prime | 781–850 | 5.2% | $473 | $3,380 |

| Prime | 661–780 | 7.0% | $495 | $4,700 |

| Non-Prime | 601–660 | 11.3% | $546 | $7,760 |

| Subprime | 501–600 | 14.8% | $591 | $10,460 |

| Deep Subprime | 300–500 | 15.7%+ | $600+ | $11,000+ |

| Credit Tier | Score Range | Average APR | Monthly Payment ($20K, 60mo) | Total Interest |

|---|---|---|---|---|

| Super Prime | 781–850 | 6.8% | $394 | $3,640 |

| Prime | 661–780 | 9.5% | $420 | $5,200 |

| Non-Prime | 601–660 | 14.5% | $469 | $8,140 |

| Subprime | 501–600 | 18.9% | $513 | $10,780 |

| Deep Subprime | 300–500 | 21.5%+ | $535+ | $12,100+ |

Key insight: A Super Prime borrower buying a $25,000 new car pays approximately $7,080 less in total interest over 60 months compared to a Subprime borrower. That’s not abstract math — it’s a number large enough to buy another used car outright.

As of Q1 2025, the average new car loan rate was 6.7% APR and the average used car loan rate was 11.9% APR according to Mercer Capital analysis. Here’s how to interpret where you stand:

Excellent rate (below 5.5% new / below 7.5% used): You’re in the top tier. You likely have a 750+ FICO score, stable income, and a strong credit history. Congratulations — you’re getting close to the best rates the market offers.

Good rate (5.5–8% new / 7.5–11% used): Solid financing that most prime borrowers achieve. You’re paying a reasonable cost for borrowing and not leaving a huge amount of money on the table.

Average rate (8–12% new / 11–15% used): You’re in the middle of the pack. If your credit has room to improve, refinancing within 12–18 months after building your score could save you meaningful money.

High rate (above 12% new / above 15% used): This is subprime territory. If you need to finance now, consider making a large down payment to reduce your principal and commit to a credit-building plan to refinance within 12 months.

Very high rate (above 15% / above 20%): Deep subprime lending. Explore alternatives — a longer credit-building period, a co-signer with better credit, or buying an older, cheaper vehicle with cash or a smaller loan.

Your credit score is the primary factor in determining your auto loan interest rate, but lenders evaluate your complete financial picture. Understanding what they assess helps you present the strongest possible application.

Your DTI is your total monthly debt payments divided by your gross monthly income. Most lenders prefer a DTI below 40–45% after including the new car payment. A high DTI can result in loan denial or a higher rate even with a good credit score.

Example: If your gross income is $6,000/month and your total monthly debts (including the new car payment) are $2,100, your DTI is 35% — typically acceptable.

LTV is your loan amount divided by the vehicle’s value. Lenders prefer LTV at or below 100%. Financing 120% of a vehicle’s value (rolling in negative equity from a trade-in) is considered high-risk and may result in a higher rate or requirement for a down payment.

Lenders generally want to see at least 2 years at your current employer (or in the same field) and documented income sufficient to support the payment. Self-employed borrowers may need to provide 2 years of tax returns.

Most lenders won’t finance vehicles older than 10 years or with more than 150,000 miles. Older vehicles command higher rates because they represent higher collateral risk — the car may not maintain its value to cover the loan if you default.

A down payment of 10–20% signals financial stability and reduces the lender’s risk by ensuring you have equity in the vehicle from day one.

Credit unions are member-owned nonprofits that typically offer the best auto loan rates in the market. Their average new car APR runs 0.5–2% below commercial banks for comparable credit profiles. You generally need to become a member (which usually requires living in a certain area, working for a specific employer, or making a small donation to an affiliated organization), but the savings are well worth the 15 minutes it takes to join.

Major banks like Chase, Bank of America, Wells Fargo, and Capital One Auto Finance offer competitive rates and the convenience of managing your loan within your existing banking relationship. Pre-approval through your bank before shopping is a smart strategy.

LightStream, AutoPay, and similar online lenders offer competitive rates with fast approvals, particularly for borrowers with good to excellent credit. They’re worth including in your rate shopping process.

Ford Motor Credit, Toyota Financial Services, GM Financial, and similar manufacturer finance arms occasionally offer promotional rates — including 0% APR — on specific models to qualified buyers. These deals are available only to buyers with 720+ credit scores and often involve choosing between the promotional rate and a cash rebate. Use a car loan comparison calculator to determine which option actually saves more money.

Dealers work with a network of lenders and markup the wholesale rate they receive (called the “buy rate”) by 1–2% as profit. This dealer reserve is legal but means you’re often paying more than you need to. Always compare dealer financing against your pre-approved rate.

Pull your free credit report from AnnualCreditReport.com and review it for errors. Disputing inaccurate negative items — which affects up to 25% of credit reports according to the FTC — can boost your score quickly.

Credit utilization (your credit card balance vs. limit) makes up 30% of your FICO score. Reducing utilization below 30% (ideally below 10%) before applying for a car loan can significantly improve your score in 30–60 days.

Each hard inquiry from a loan application temporarily reduces your score. Give your credit time to stabilize before applying for auto financing.

A down payment of 20% not only reduces your monthly car payment and total interest — it reduces lender risk, which can improve your offered rate by 0.25–0.5%.

Rate shopping within a 14–45 day window counts as a single hard inquiry for FICO scoring purposes, so apply to 3–5 lenders without fear. Compare each pre-approval using a car loan interest calculator to find the actual lowest-cost offer.

If your credit is poor, adding a creditworthy co-signer — a parent, spouse, or relative with 720+ credit — can dramatically improve your offered rate. Be aware that both parties are equally responsible for the loan.

A trade-in reduces your loan principal like a down payment. Even a modest trade-in reduces the amount you need to finance and can positively affect your LTV ratio.

Buyers often brush off a 1% difference in APR as “not that big a deal.” The numbers disagree:

$25,000 loan, 60 months:

$35,000 loan, 72 months:

A single percentage point on a larger, longer loan easily costs over $1,000. This is why negotiating your APR — not just your monthly payment — is the most financially impactful thing you can do during the car-buying process.

Used car loans consistently carry higher APRs than new car loans. There are two main reasons:

Collateral risk: A used vehicle has already experienced its sharpest depreciation. Its future value is less predictable, making it riskier collateral from the lender’s perspective. A new car has a manufacturer warranty, consistent demand, and more predictable resale value.

Borrower profile: Used car buyers — particularly those shopping at independent dealers — statistically have lower credit scores on average than new car buyers. Lenders price their risk accordingly.

This is important for used car loan shoppers: the used car loan calculator in your budgeting process should use a rate that’s 2–4% higher than what you might see advertised for new vehicles. Many buyers are surprised to find their used car loan rate is significantly higher than expected.

Refinancing makes the most sense when:

Use the refinance auto loan calculator feature in our comparison tool — enter your current remaining balance and rate vs. a new offer — to see exactly how much you’d save before making the decision.

| Day | Action |

|---|---|

| Day 1 | Pull credit report, identify and dispute any errors |

| Day 7–30 | Pay down credit card balances, avoid new accounts |

| Day 30–45 | Get pre-approved by credit union |

| Day 45–60 | Get pre-approved by 1–2 banks or online lenders |

| Day 60–75 | Visit dealerships with pre-approvals in hand |

| Day 75–90 | Negotiate vehicle price first, then compare financing offers |

| Post-purchase | Monitor credit; consider refinancing in 12–18 months if rates improve |

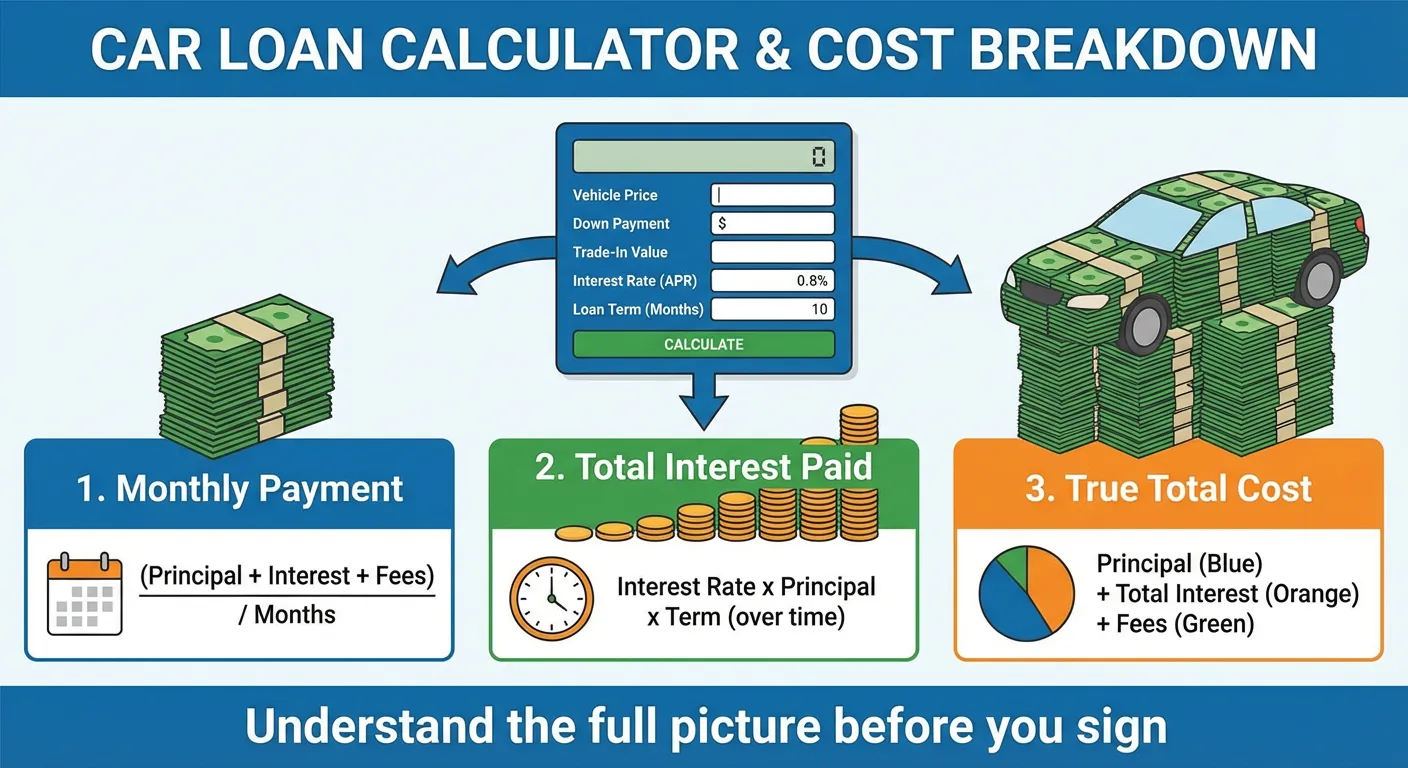

Use our free Auto Loan Rate Calculator to see your exact monthly payment and total interest at any APR.