11

11

Your monthly car payment is the number dealers want you to focus on. It is the number they negotiate around, the number they stretch to make any car seem affordable, and the number that hides the true cost of your purchase.

This guide explains how car monthly payments are calculated, what variables control them, and how to use a car payment calculator intelligently — so you never walk into a showroom without knowing exactly what you should be paying.

Calculate Your Monthly Car Payment →

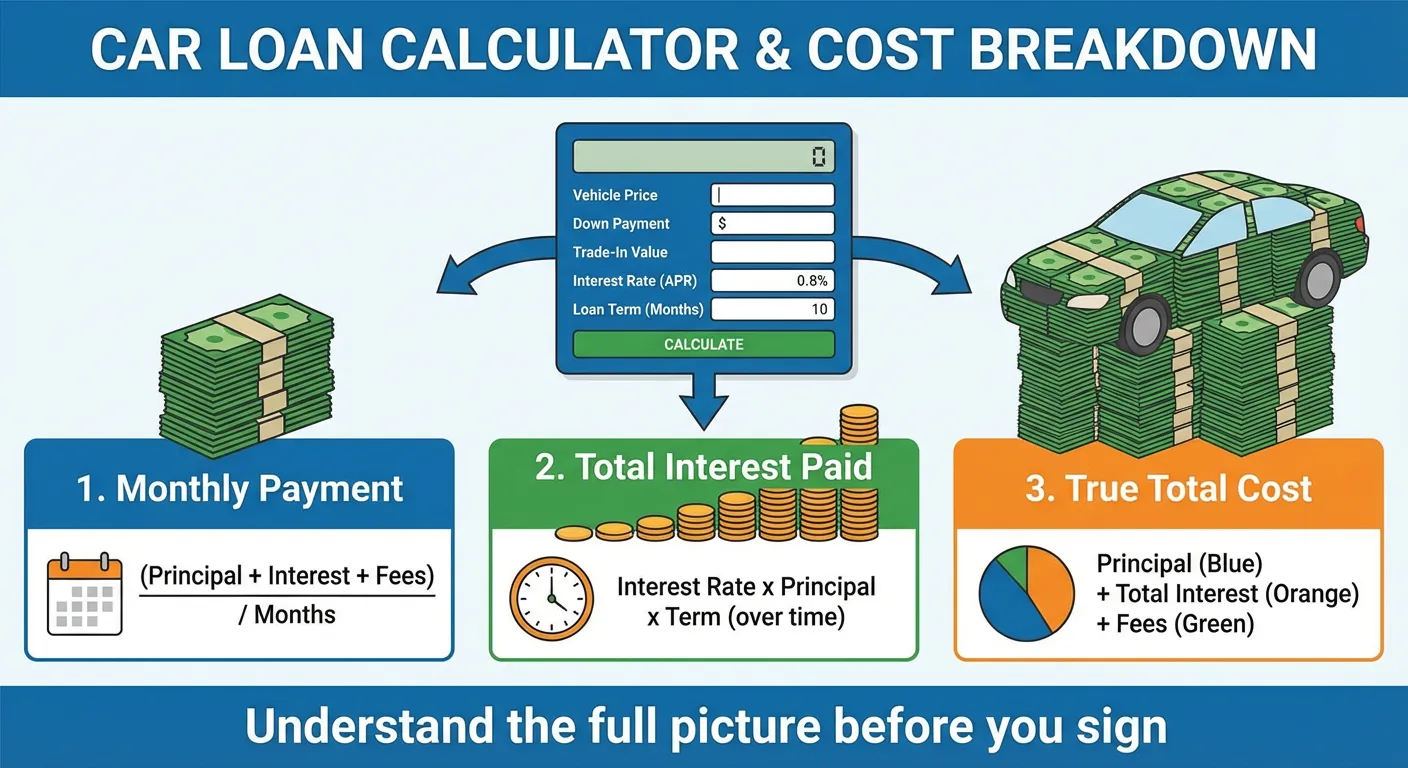

A car monthly payment is the fixed amount you pay to a lender each month over the life of your auto loan. It is calculated based on four variables:

The payment itself does not change month to month. But what the payment is made up of — how much goes to interest versus how much reduces your balance — changes every single month.

A car payment calculator takes your inputs and applies the standard amortization formula to produce your exact monthly payment.

The core inputs are:

Many calculators also include:

The output is your monthly payment, total interest paid, total amount paid over the life of the loan, and often a full amortization schedule showing every payment broken down.

The single biggest driver of your monthly payment is how much you borrow. Reducing the loan principal through a larger down payment, a meaningful trade-in, or simply buying a less expensive vehicle has a more powerful effect on your monthly payment than almost any other factor.

Here is how principal affects monthly payment at 7% APR over 60 months:

| Loan Amount | Monthly Payment | Total Interest |

|---|---|---|

| $15,000 | $297 | $2,816 |

| $20,000 | $396 | $3,755 |

| $25,000 | $495 | $4,694 |

| $30,000 | $594 | $5,633 |

| $35,000 | $693 | $6,572 |

| $40,000 | $792 | $7,511 |

| $45,000 | $891 | $8,450 |

Every $5,000 reduction in loan amount saves approximately $99/month and $939 in interest on a 60-month loan at 7%.

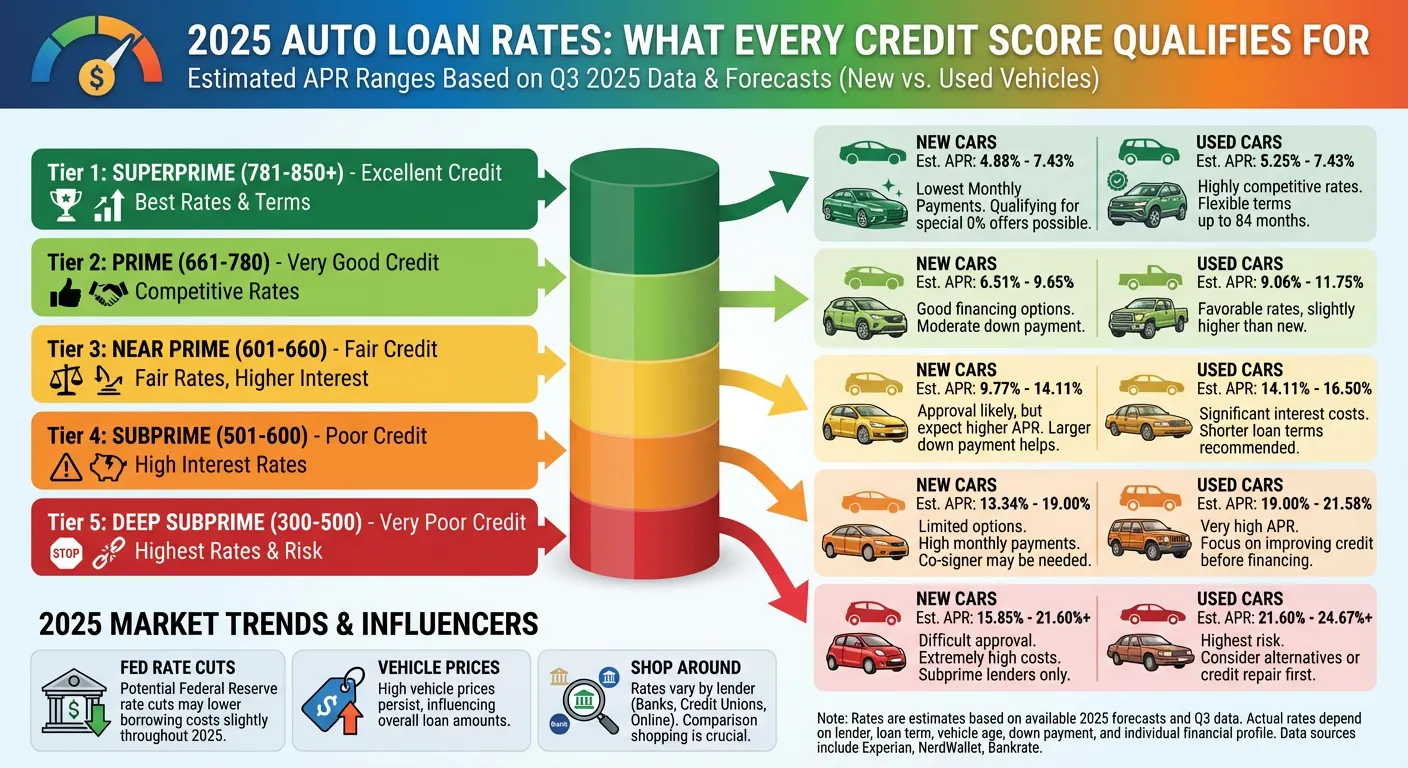

Your APR is determined primarily by your credit score and secondarily by current market conditions. It is the variable most buyers have some control over — by improving credit before applying, shopping multiple lenders, and negotiating rather than accepting the first offer.

Impact of APR on a $28,000 loan over 60 months:

| APR | Monthly Payment | Total Interest | Difference from 5% |

|---|---|---|---|

| 5.0% | $529 | $3,720 | — |

| 6.0% | $541 | $4,473 | +$753 |

| 7.0% | $554 | $5,233 | +$1,513 |

| 8.0% | $567 | $6,001 | +$2,281 |

| 10.0% | $595 | $7,562 | +$3,842 |

| 12.0% | $623 | $9,163 | +$5,443 |

| 15.0% | $666 | $11,956 | +$8,236 |

The difference between a 5% and 15% APR on this loan is $137/month and $8,236 in total interest paid over five years. For the exact same car.

Loan term is where dealers most commonly manipulate monthly payment. By extending a loan from 60 to 84 months, a dealer can lower your payment by $100–$200 per month — which makes a car that is $5,000–$8,000 outside your budget suddenly appear to fit.

But here is the hidden cost:

$32,000 car, 7% APR, different terms:

| Term | Monthly Payment | Total Interest | End Balance at 30 months |

|---|---|---|---|

| 36 months | $988 | $3,562 | $0 (paid off) |

| 48 months | $766 | $4,773 | $16,900 owed |

| 60 months | $634 | $6,018 | $19,800 owed |

| 72 months | $548 | $7,439 | $22,200 owed |

| 84 months | $486 | $8,802 | $23,900 owed |

The 84-month loan has you still owing $23,900 in month 30 — on a vehicle that is now 2.5 years old and likely worth $20,000–$22,000. You are underwater, and significantly so.

Your down payment reduces the loan amount from the start. It also demonstrates financial responsibility to lenders, which can sometimes improve your offered APR. And it provides an immediate buffer against depreciation.

Effect of down payment on $30,000 car, 7% APR, 60 months:

| Down Payment | Loan Amount | Monthly Payment | Total Interest |

|---|---|---|---|

| $0 (0%) | $30,000 | $594 | $5,633 |

| $1,500 (5%) | $28,500 | $565 | $5,351 |

| $3,000 (10%) | $27,000 | $535 | $5,069 |

| $6,000 (20%) | $24,000 | $475 | $4,505 |

| $9,000 (30%) | $21,000 | $416 | $3,940 |

Going from 0% to 20% down reduces monthly payment by $119 and saves $1,128 in interest.

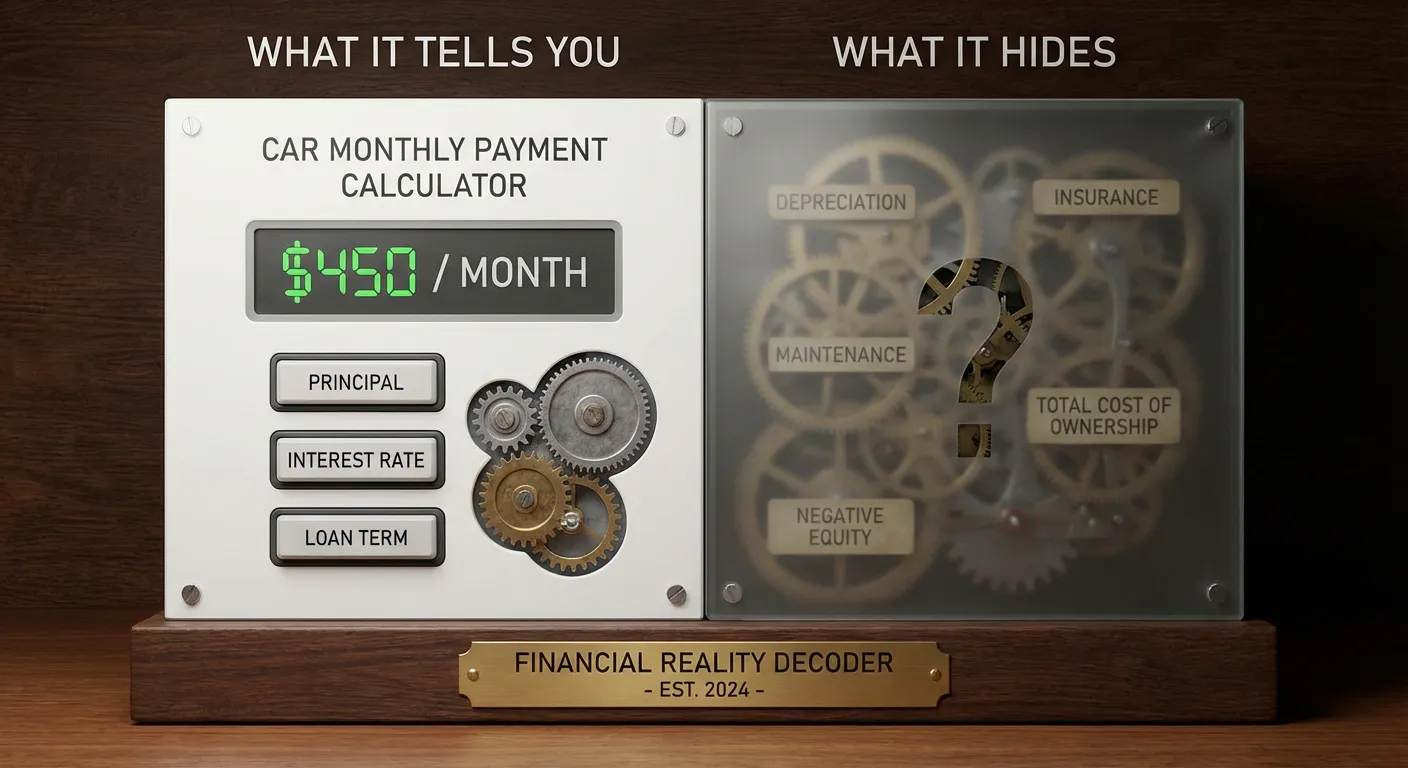

Here is the thing about monthly car payments that dealers rely on you not noticing: the payment tells you almost nothing about whether you can truly afford the car.

The monthly payment says nothing about:

Total interest cost. A $600/month payment on a 48-month loan costs $28,800 total. The same $600/month on a 72-month loan — which a dealer might offer to make a more expensive car “fit” your budget — could cost $43,200 total.

Insurance cost. A $600/month loan payment on a $35,000 vehicle will be accompanied by full coverage insurance requirements. In many markets, that is $150–$250/month more — a total real-world payment of $750–$850/month, not $600.

Operating costs. Fuel, maintenance, and registration add another $350–$600/month for most drivers. Your true monthly car expense is often $400–$600 more than the loan payment alone.

Depreciation. That $35,000 car is worth roughly $28,000 after 12 months. You cannot see depreciation in a payment — it only becomes real when you try to sell or trade in and discover you owe more than the car is worth.

A complete car monthly payment calculator accounts for all of these elements. A basic payment calculator shows you only what you owe the bank.

Rather than finding a car you like and calculating the payment, work in reverse:

Step 1: Determine your maximum monthly payment Take your monthly take-home pay and multiply by 15%. That is the upper limit of your car payment. Example: $4,500 take-home × 0.15 = $675 maximum payment

Step 2: Subtract insurance estimate Full coverage insurance on a financed vehicle: estimate $150–$200/month $675 – $175 (insurance) = $500 for the loan payment itself

Step 3: Work backwards to find your maximum loan amount At 7% APR over 60 months, a $500/month payment supports a loan of approximately $25,200.

Step 4: Add your down payment for maximum vehicle price If you have $4,000 for a down payment: $25,200 + $4,000 = approximately $29,200 vehicle price before taxes and fees.

Step 5: Account for taxes and fees At 8% sales tax + $600 in fees on a $29,200 car, taxes and fees add $2,936 + $600 = $3,536, which either increases your loan or requires additional cash.

This reverse calculation gives you a real maximum car price before you ever look at a single vehicle.

| Annual Income | Take-Home (est.) | Max Car Payment (15%) | Max Loan Amount (7%, 60 mo) | Max Car Price (10% down) |

|---|---|---|---|---|

| $30,000 | $2,100 | $315 | $15,850 | $17,600 |

| $40,000 | $2,800 | $420 | $21,100 | $23,500 |

| $50,000 | $3,400 | $510 | $25,650 | $28,500 |

| $60,000 | $4,050 | $607 | $30,550 | $33,950 |

| $75,000 | $4,950 | $742 | $37,350 | $41,500 |

| $90,000 | $5,900 | $885 | $44,550 | $49,500 |

| $100,000 | $6,500 | $975 | $49,100 | $54,600 |

| $125,000 | $8,000 | $1,200 | $60,400 | $67,100 |

These assume moderate existing debt. Use our car payment calculator to run your exact scenario.

Never tell a dealer what monthly payment you are targeting. The moment you reveal your payment ceiling, they will work backwards from that number to justify whatever vehicle price serves them best — by adjusting the term length, not the price.

Always negotiate the out-the-door price first. Then, and only then, discuss financing separately.

Dealer financing is convenient but rarely competitive. Get pre-approved from your credit union or bank before visiting. Your pre-approval gives you a benchmark that dealer financing must beat to earn your business. Even when dealer financing rates are comparable, having a competing offer in hand gives you leverage.

Every month of additional loan term is a month of additional interest. Extending from 60 to 84 months to save $100/month costs you $2,000–$4,000 more in total interest depending on your loan size and rate. It also keeps you underwater on the loan for longer, limiting your flexibility to sell, trade, or refinance.

If $100/month is the difference between affording the car and not affording it, the honest answer is that the car is not in your budget — at least not yet.

A $32,000 car with 8% sales tax and $800 in doc and registration fees has an out-the-door price of $35,360. If you are financing everything, your loan is $35,360 minus your down payment — not $32,000 minus your down payment. Many buyers are surprised when their payment is $60–$80 higher than expected because they calculated based on the vehicle price, not the financed amount.

A good car payment calculator lets you run multiple scenarios side by side. Here are the most useful comparisons to make:

Short term vs. long term: Same vehicle, same APR — compare 48, 60, 72 month payments and total costs. Decide whether the monthly savings are worth the additional interest.

More down vs. less down: Calculate the payment with 5%, 10%, and 20% down. This shows exactly how much each additional dollar of down payment reduces your monthly obligation.

Buying vs. waiting to improve credit: Calculate current payment at your current APR, then calculate what the payment would be with a 720+ credit score and a 2% lower APR. If the difference is significant, quantify exactly how much you save by waiting 6 months to improve your credit.

Extra payment impact: Calculate your standard payment, then use the extra payment feature to see how much interest you save and how many months earlier you pay off the loan by adding $50, $100, or $200 extra per month.

To truly understand whether a car fits your budget, your car payment calculator results should be combined with these additional monthly costs:

| Cost Category | Average Monthly Range |

|---|---|

| Loan payment | $300 – $900 |

| Auto insurance (full coverage) | $120 – $250 |

| Fuel | $100 – $300 |

| Routine maintenance reserve | $50 – $150 |

| Registration / annual fees | $25 – $75 |

| Parking and tolls | $0 – $200 |

| Total Monthly Car Cost | $595 – $1,875 |

For most buyers, the true all-in monthly cost of car ownership is $800–$1,300/month. Staying within 20% of your monthly take-home pay for this total figure keeps your car from dominating your financial life.

If you are buying a car with cash, there is no monthly loan payment — but there is still a real monthly cost of car ownership.

For cash buyers, the relevant monthly calculation is:

Monthly opportunity cost + Insurance + Fuel + Maintenance

The opportunity cost is what that cash could have earned in an investment account. If you spend $25,000 cash on a car, and that money could have earned 7% annually invested, the opportunity cost is roughly $145/month in foregone returns.

This does not mean cash purchases are bad — avoiding interest payments is valuable. But it is worth calculating whether the interest you save is worth more or less than the investment returns you give up. Our cash vs. financing calculator handles this comparison automatically.

The most powerful thing you can do as a car buyer is know your maximum monthly payment — and the maximum vehicle price it supports — before you see a single car on a lot. When you know your number, no dealer tactic, no extended test drive, and no shiny feature package can move you outside your budget.

Use our car monthly payment calculator to work forwards (payment from price) or backwards (price from payment). Enter your income, your down payment, your estimated APR based on credit score, and your preferred loan term. Know your number. Then go shopping.

Calculate Your Monthly Car Payment →