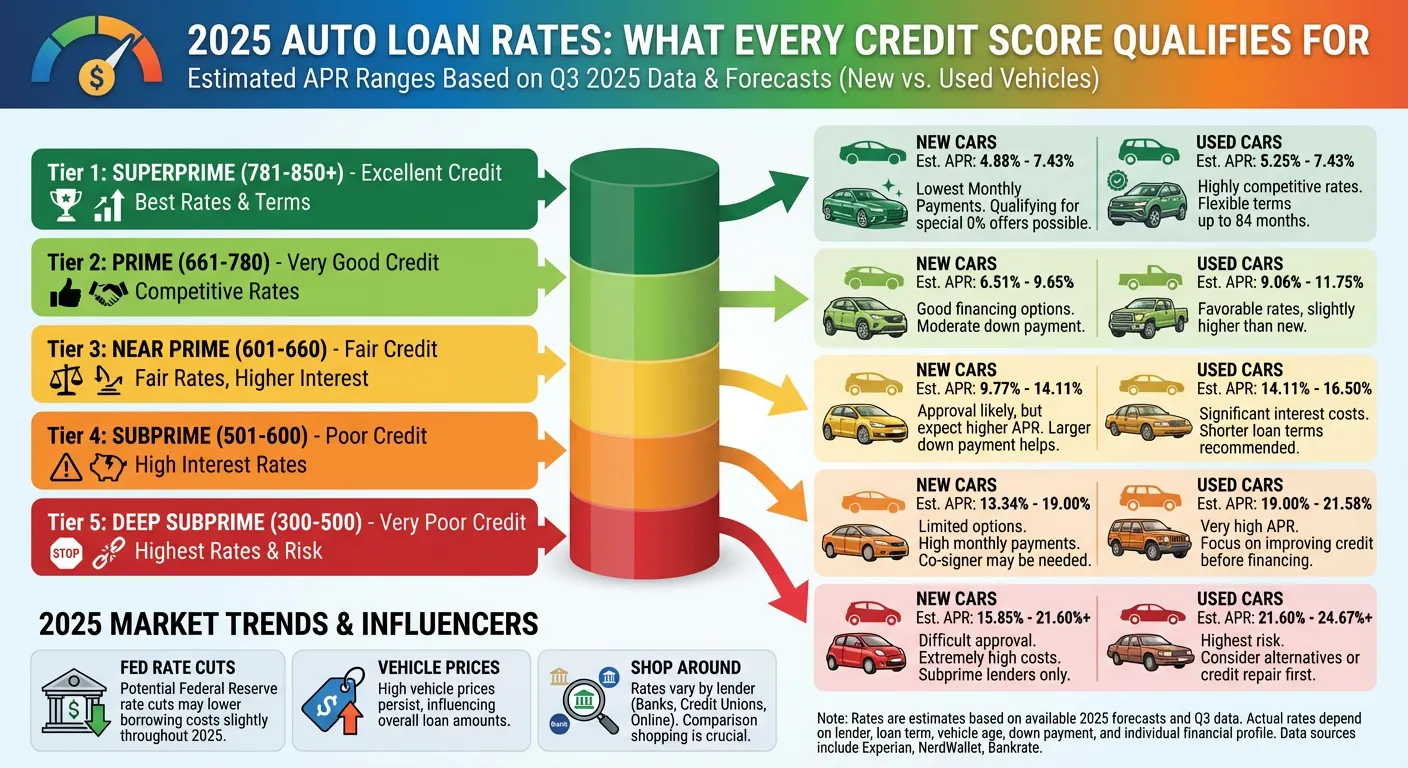

11

11

Two people can buy the exact same car at the exact same price and end up with very different financial outcomes — simply based on whether they paid cash or financed, and how they managed that decision.

This guide breaks down the real math behind paying cash versus financing a car, how to calculate your true total cost of ownership over the years you drive it, and which choice makes more financial sense for different buyers.

Paying cash for a car feels financially virtuous. No debt, no interest, no monthly obligation. And in many situations, it genuinely is the smarter choice.

But in others — particularly when interest rates are low and the cash could earn meaningful returns invested elsewhere — financing actually beats paying cash on pure numbers.

The answer depends on three variables:

The most obvious benefit. A $28,000 car purchased with cash costs $28,000. The same car financed at 8% APR over 60 months costs $34,055 in total — $6,055 more for the privilege of paying over time.

That $6,055 is guaranteed lost money. There is no scenario where paying $6,055 in loan interest is better than having paid nothing.

The car loan industry has a well-documented history of expensive add-ons, rate markups, and term extensions that cost buyers thousands of dollars. Cash buyers are immune to all of it. You negotiate price, write a check, drive away. No financing paperwork, no dealer F&I office pressure, no opportunity for rate manipulation.

No car payment means $400–$700/month freed up for savings, investment, debt payoff, or anything else. This simplification of cash flow is genuinely valuable, particularly for buyers with variable income or irregular expenses.

A financed car can leave you owing more than the car is worth — especially in the early years of a loan and especially if you put little or nothing down. A cash purchase means you own the car outright from day one. You can sell it any time for whatever the market will pay, without needing to clear a loan balance first.

If you can earn 7%–10% investing your cash (S&P 500 index funds have returned approximately 10% annually over long historical periods), and your car loan only costs 5%–6% in interest — mathematically, you come out ahead by financing and investing the difference.

Let’s put actual numbers on this:

Scenario A — Pay cash for $28,000 car

Scenario B — Finance at 6% APR, invest $28,000 at 7%

In this scenario, financing wins by $6,840 over 5 years — because the investment return exceeds the loan interest cost.

However: this analysis assumes you actually invest the money, the market delivers expected returns, and your loan rate is below your investment return. These are meaningful assumptions.

If you have high-interest debt — credit cards at 20%+, personal loans at 12%+ — putting $28,000 toward a car instead of eliminating that debt is almost certainly the wrong financial move. Finance the car at 7% and use your cash to eliminate the 20% credit card debt first.

Sometimes manufacturers offer 0% or sub-2% APR on new vehicles to drive sales. When this is available, there is no financial argument for paying cash — financing at 0% cost you nothing while keeping your cash available.

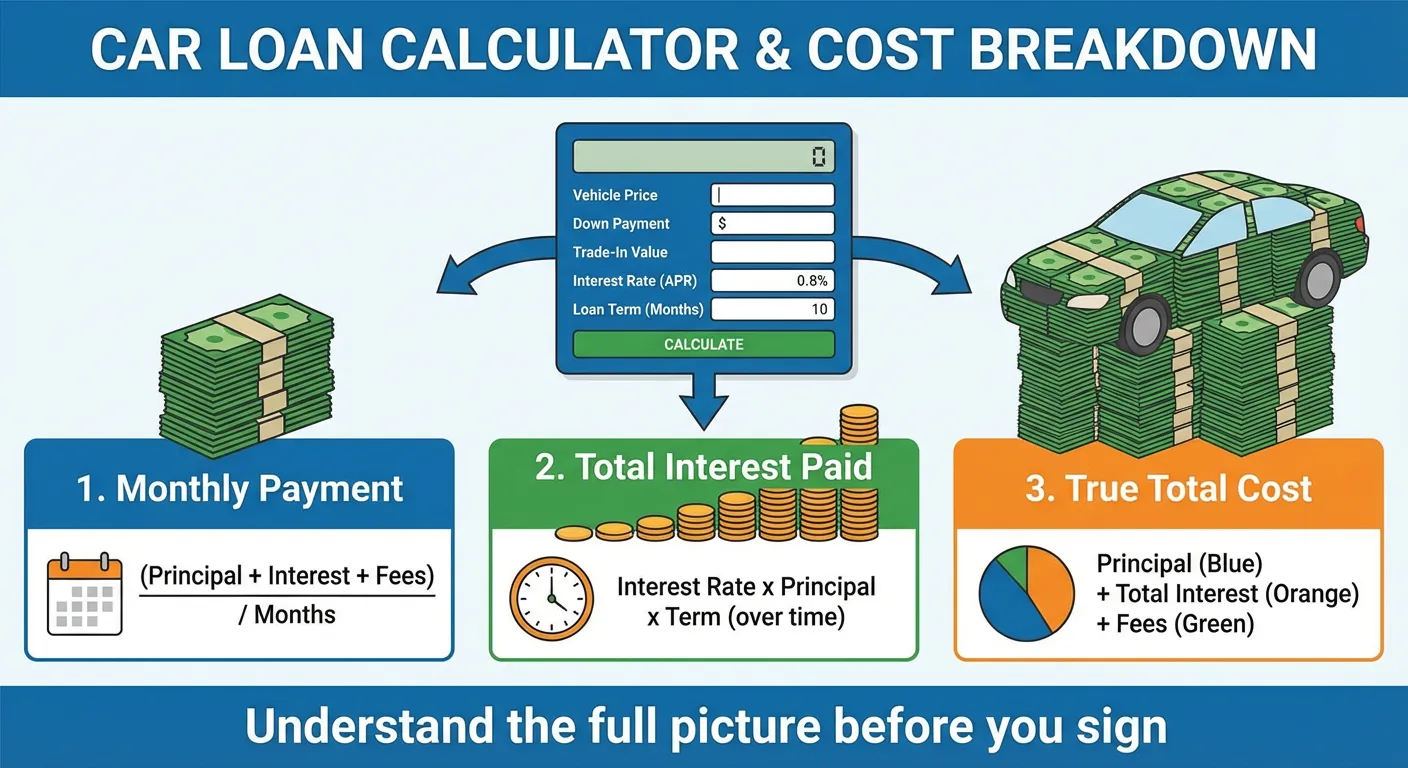

Monthly payment and purchase price are just two of the eight meaningful cost categories of owning a car. To understand what a vehicle truly costs, you need to calculate all of them.

The starting point. Include the full out-the-door price: negotiated vehicle price + sales tax + doc fees + registration + any dealer add-ons.

On a $30,000 car with 8% tax and $700 in fees, the out-the-door price is $33,100.

If you finance, the total interest paid over the loan term is a real cost of ownership. On $33,100 at 7% APR over 60 months, total interest is approximately $6,233.

Depreciation is the largest and most overlooked cost of owning a new car. It is not a cash payment you make — but it is real money you lose.

A $30,000 car that is worth $15,000 after 5 years has cost you $15,000 in depreciation — $3,000/year or $250/month in lost value. That is often more than the monthly loan interest payment.

Depreciation estimates by vehicle category:

| Vehicle Type | Year 1 Loss | 5-Year Loss | Retained at 5 Years |

|---|---|---|---|

| Economy sedan | 18% | 47% | 53% |

| Midsize sedan | 20% | 52% | 48% |

| Compact SUV | 19% | 49% | 51% |

| Full-size SUV | 22% | 56% | 44% |

| Luxury sedan | 28% | 63% | 37% |

| Electric vehicle | 25% | 55% | 45% |

| Pickup truck | 15% | 41% | 59% |

Pickup trucks and economy vehicles retain value best. Luxury vehicles depreciate fastest — which is why buying a 2-3 year old luxury vehicle is often spectacular value.

Full coverage insurance (required by lenders) costs an average of $1,500–$2,400/year depending on:

Over five years, insurance typically costs $7,500–$12,000 — often more than the loan interest paid.

Annual fuel cost depends on your miles driven, your vehicle’s MPG, and local gas prices.

Simple formula: (Annual miles ÷ MPG) × average gas price = annual fuel cost

At 15,000 miles/year, $3.50/gallon:

Over 5 years, the difference between a 25 MPG and 32 MPG vehicle is approximately $2,295 in fuel costs. Not dramatic, but real.

Routine maintenance — oil changes, tire rotations, air filters, brake pads, tires — runs $800–$1,500/year for most vehicles in good condition. New vehicles under warranty have lower maintenance costs; older vehicles and those with high mileage have higher ones.

Budget breakdown for a typical vehicle:

| Service | Frequency | Annual Cost Estimate |

|---|---|---|

| Oil changes | 2–4x/year | $120 – $320 |

| Tire rotation | 2x/year | $40 – $80 |

| New tires | Every 3–5 years | $200 – $400/year |

| Brake pads | Every 3–5 years | $100 – $200/year |

| Filters, belts, fluids | As needed | $100 – $300/year |

| Unexpected repairs | Variable | $200 – $800/year |

| Total Annual Maintenance | — | $760 – $2,100 |

Annual registration fees vary enormously by state and vehicle value. Nevada, for example, charges based on vehicle value (from $80 to $600+/year). Florida charges flat fees under $100 for most vehicles. California charges a percentage of vehicle value.

Budget $400–$1,200/year in the first few years, declining as the vehicle depreciates.

Often overlooked but real. In urban areas, monthly parking can cost $100–$400. Tolls vary widely by commute. If you are buying a car partly for a commute that involves regular tolls, these need to be in your total cost calculation.

Here is the complete 5-year cost for three common vehicle types:

Economy Compact — $22,000 purchase price

| Cost Category | Total (5 Years) |

|---|---|

| Purchase + tax + fees | $24,400 |

| Loan interest (7%, 60 mo, $4,000 down) | $4,800 |

| Depreciation (47%) | $10,340 |

| Insurance | $7,500 |

| Fuel (15k mi/yr, 34 mpg, $3.50) | $7,720 |

| Maintenance | $5,000 |

| Registration | $1,800 |

| Less resale value | -$11,660 |

| True 5-Year Cost | $49,900 |

Midsize SUV — $38,000 purchase price

| Cost Category | Total (5 Years) |

|---|---|

| Purchase + tax + fees | $42,200 |

| Loan interest (7%, 60 mo, $5,000 down) | $8,900 |

| Depreciation (49%) | $18,620 |

| Insurance | $10,500 |

| Fuel (15k mi/yr, 28 mpg, $3.50) | $9,375 |

| Maintenance | $5,500 |

| Registration | $3,000 |

| Less resale value | -$19,380 |

| True 5-Year Cost | $78,715 |

Luxury Sedan — $58,000 purchase price

| Cost Category | Total (5 Years) |

|---|---|

| Purchase + tax + fees | $64,200 |

| Loan interest (6%, 60 mo, $10,000 down) | $10,800 |

| Depreciation (63%) | $36,540 |

| Insurance | $15,000 |

| Fuel (15k mi/yr, 26 mpg, $3.50) | $10,096 |

| Maintenance | $9,500 |

| Registration | $5,500 |

| Less resale value | -$21,460 |

| True 5-Year Cost | $130,176 |

These numbers are striking. The midsize SUV’s true 5-year cost is $78,715 — nearly $16,000 more per year than the compact. The luxury sedan costs $130,176 over five years — $26,000 per year just to own and drive.

Here is a clean decision framework based on your car loan APR versus your expected investment return:

| Your Car Loan APR | S&P 500 Historical Avg (~10%) | Verdict |

|---|---|---|

| Under 4% | 10% | Finance — clear mathematical winner |

| 4% – 6% | 10% | Finance — meaningful advantage |

| 6% – 8% | 10% | Financing still wins, but margin shrinks |

| 8% – 10% | 10% | Very close — personal preference decides |

| Over 10% | 10% | Pay cash — guaranteed savings beat uncertain returns |

| Any rate | Conservative 5% return | Finance only if APR is below 5% |

The honest caveat: investment returns are not guaranteed. A 7% car loan and a 10% expected return looks good mathematically — until the market has a bad 5 years. Cash buyers face no such uncertainty.

Running this calculation manually is time-consuming and easy to get wrong. Our cash vs. financing calculator lets you enter your purchase price, loan terms, estimated investment return rate, and years of ownership — and instantly shows you which option comes out ahead and by exactly how much.

It also calculates your full five-year total cost of ownership including depreciation estimates, so you see the complete financial picture of any vehicle you are considering buying — whether you plan to pay cash or finance.

Make the calculation before you commit. The numbers tell the truth, even when emotions point another direction.

[Calculate Cash vs. Financing for Your Car →]

Pay cash when:

Finance when:

The universal rule: Never stretch your budget to buy more car than you can afford, regardless of whether you are paying cash or financing. The most expensive car is always the one that disrupts your financial stability.