11

11

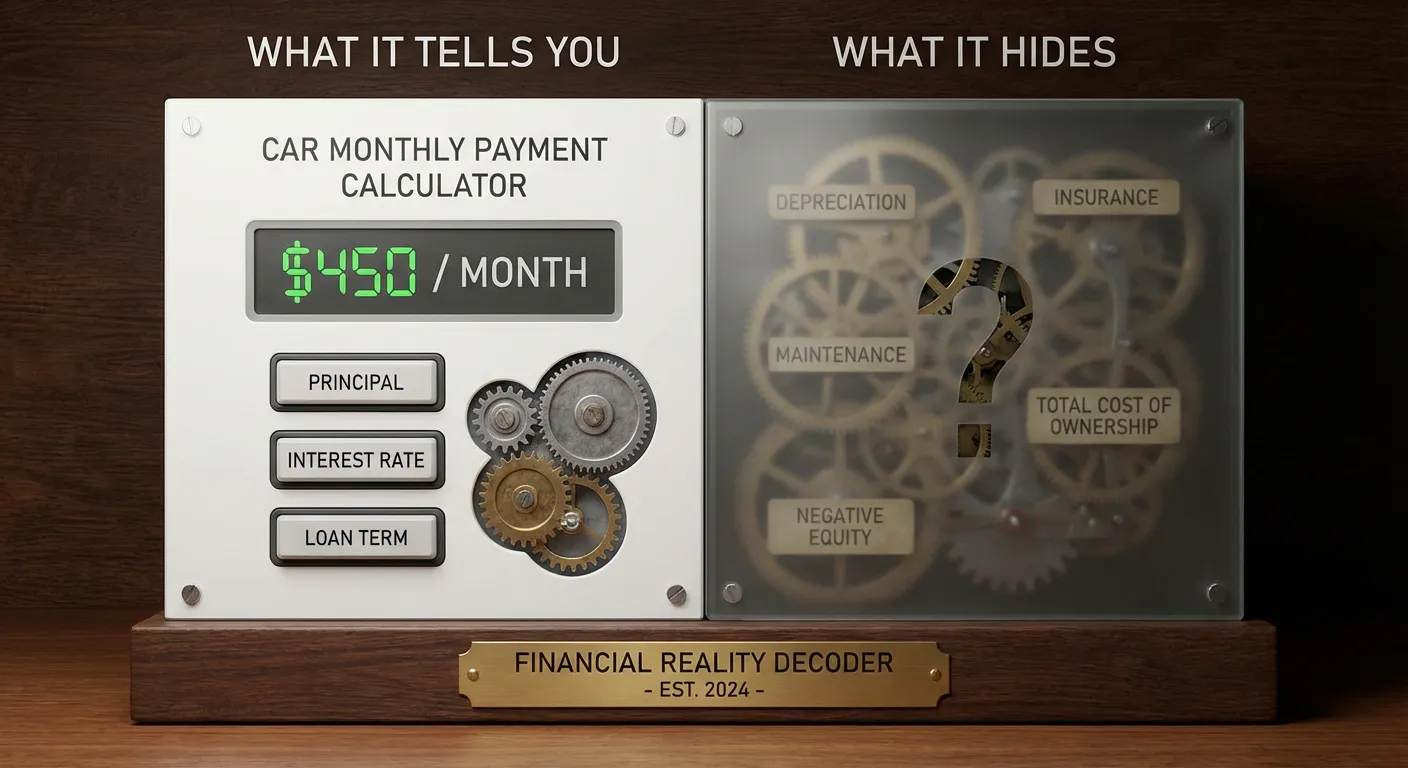

Most people only see one number when they are buying a car — the monthly payment. But that single number hides the real story. Understanding how car loan interest works, how to calculate your true total cost, and how small changes in APR, term, and down payment can save or cost you thousands of dollars — that knowledge is the difference between a smart car purchase and an expensive one.

This complete guide to car loan calculation covers everything you need to know before you sign a single piece of financing paperwork.

A car loan is a type of installment loan. You borrow a specific amount of money (the principal), agree to repay it over a set period (the term), and pay interest on the outstanding balance each month.

Unlike simple interest on a savings account, auto loan interest is calculated using an amortization schedule. This means your early payments are mostly interest, and your later payments are mostly principal. The lender front-loads the interest so that if you pay off the loan early or sell the car, they have already collected the bulk of their profit.

Here is a concrete example. On a $25,000 loan at 7% APR over 60 months, your monthly payment is $495.

By the time you are making your final payments, almost all of your money is reducing what you owe. But in the beginning, you are mostly paying the bank.

The formula lenders use to calculate your monthly payment is:

M = P × [r(1+r)^n] / [(1+r)^n – 1]

Where:

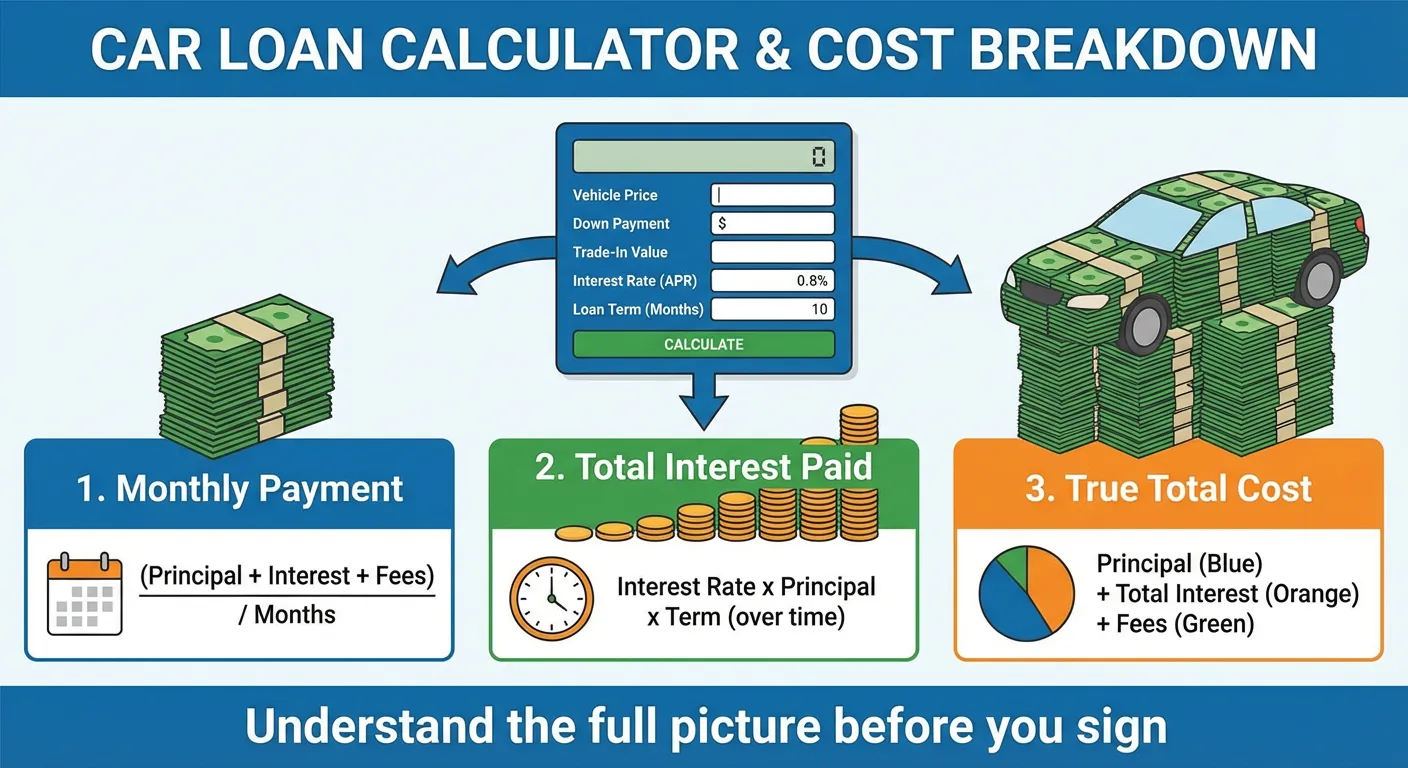

If math is not your thing, our car loan calculator handles all of this instantly. Enter your loan amount, interest rate, and term — the calculator returns your exact monthly payment, total interest paid, total amount paid, and a complete month-by-month amortization schedule.

Your loan amount is not simply the sticker price of the car. It is the out-the-door price minus your down payment and trade-in equity, plus any fees rolled into the loan.

Out-the-door price includes:

Minus:

This final number is your actual loan amount — and it is often $2,000–$5,000 higher than buyers expect, which is why pre-calculating it before visiting a dealer is so important.

Your annual percentage rate (APR) is one of the two most powerful variables in your car loan. Even a 1% difference in APR has a significant impact on total cost over a 5- or 6-year loan.

Here is what different APRs cost on a $28,000 car loan over 60 months:

| APR | Monthly Payment | Total Interest | Total Cost |

|---|---|---|---|

| 3.9% | $515 | $2,888 | $30,888 |

| 5.9% | $540 | $4,376 | $32,376 |

| 7.9% | $566 | $5,947 | $33,947 |

| 9.9% | $593 | $7,591 | $35,591 |

| 12.9% | $636 | $10,155 | $38,155 |

| 16.9% | $697 | $13,802 | $41,802 |

The difference between a 3.9% APR (excellent credit) and 16.9% APR (poor credit) on this same loan is $182 per month and $10,914 in total interest paid. That is nearly $11,000 extra for the exact same car.

This is why your credit score is so important before buying a car. Improving your score from poor to excellent before applying for a car loan can save you more money than nearly any negotiation tactic.

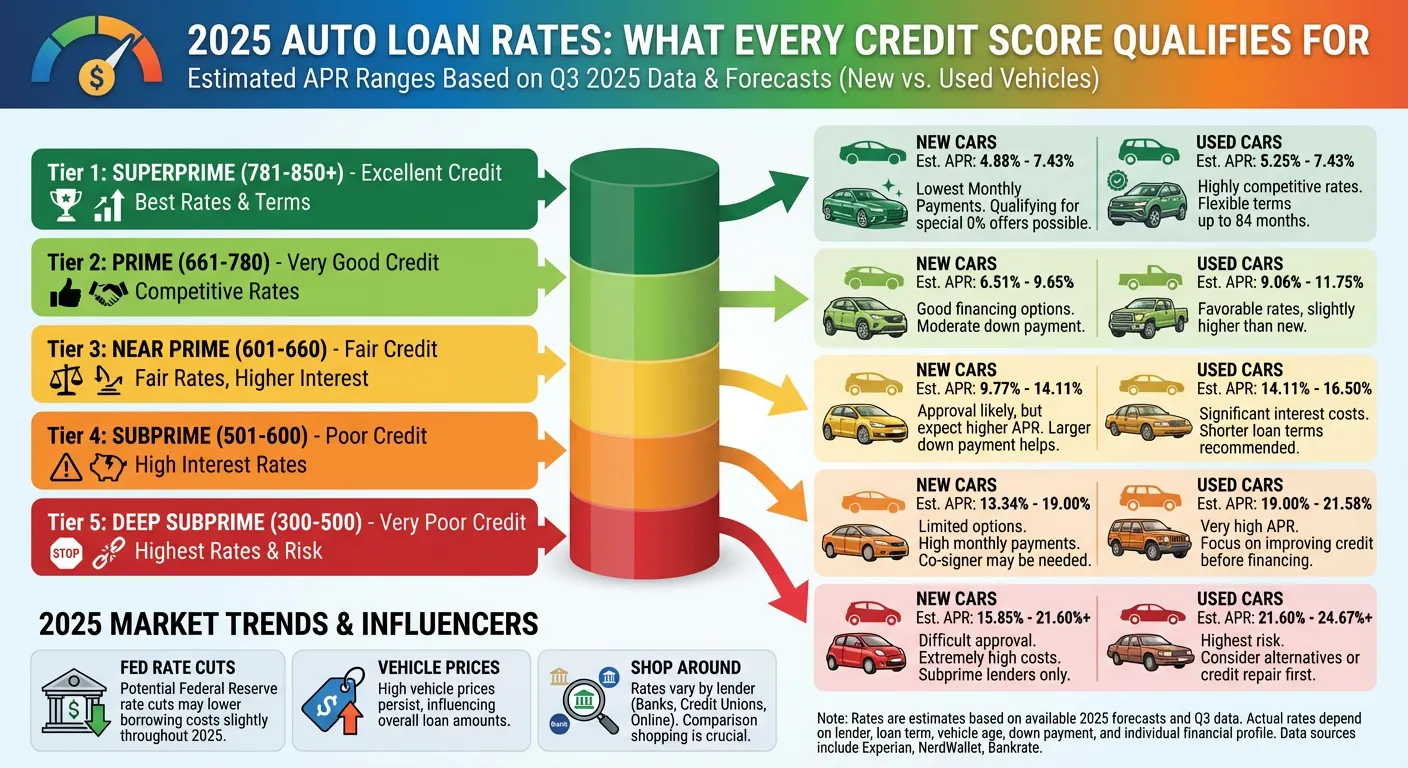

Lenders use credit score tiers to assign interest rates. While exact rates change with market conditions, here is a representative picture of current auto loan rate tiers:

| Credit Score Range | Credit Tier | Typical New Car APR | Typical Used Car APR |

|---|---|---|---|

| 781 – 850 | Super Prime | 4.5% – 5.5% | 5.5% – 6.5% |

| 661 – 780 | Prime | 6.0% – 7.5% | 7.0% – 9.0% |

| 601 – 660 | Near Prime | 8.5% – 11.0% | 10.0% – 13.5% |

| 501 – 600 | Subprime | 12.0% – 16.0% | 14.0% – 18.0% |

| 300 – 500 | Deep Subprime | 16.0% – 24.0% | 18.0% – 26.0% |

If your credit score is below 660, the best financial move may be to delay the car purchase by 6–12 months, aggressively pay down credit card balances, and allow your score to climb into the prime tier before applying. The interest savings almost always outweigh the inconvenience.

Loan term is the second major variable in your car loan. Longer terms lower monthly payments but dramatically increase total cost. Here is the full comparison on a $22,000 loan at 7% APR:

| Term | Monthly Payment | Total Interest | Total Paid | Savings vs. 84-mo |

|---|---|---|---|---|

| 24 months | $988 | $1,715 | $23,715 | $4,521 |

| 36 months | $679 | $2,454 | $24,454 | $3,782 |

| 48 months | $526 | $3,227 | $25,227 | $3,009 |

| 60 months | $435 | $4,082 | $26,082 | $2,154 |

| 72 months | $376 | $5,044 | $27,044 | $1,192 |

| 84 months | $334 | $6,236 | $28,236 | — |

The 84-month loan saves $654 per month compared to the 24-month loan. But it costs $4,521 more in total interest. That is a significant premium for the convenience of a lower monthly payment.

The general recommendation from financial advisors: Never take a loan longer than 60 months for a new car, and no longer than 48 months for a used car. Beyond these lengths, depreciation risk increases significantly — especially on used vehicles.

Used car loans almost always carry higher interest rates than new car loans. There are two reasons: used cars are harder to value precisely (creating more lender risk), and used cars are more likely to have mechanical problems, increasing the chance of default.

Typical spread: used car APR runs 1%–3% higher than new car APR for the same borrower.

Many lenders impose shorter maximum terms on older vehicles. A car that is 5 years old may only qualify for a 48-month loan, while a brand-new car can be financed for 84 months.

Lenders set loan-to-value (LTV) limits on used car financing. If a used car’s market value is $15,000, a lender offering 100% LTV will loan up to $15,000. But if you are paying above market value, you may only receive a loan for the appraised value — leaving you to cover the difference in cash.

If you want to verify the numbers yourself before using a calculator, here is the process:

Step 1: Determine your out-the-door price Vehicle price: $30,000 Sales tax (8%): $2,400 Doc fee: $395 Registration: $250 Total out-the-door: $33,045

Step 2: Subtract down payment and trade-in Down payment: -$5,000 Trade-in equity: -$3,000 Net trade-in (trade-in minus payoff): -$2,500 Amount to finance: $25,545

Step 3: Calculate monthly payment APR: 7.5% Term: 60 months Monthly rate (r): 7.5% ÷ 12 = 0.625% = 0.00625 Monthly payment: $25,545 × [0.00625 × (1.00625)^60] ÷ [(1.00625)^60 – 1] = $25,545 × [0.00625 × 1.4535] ÷ [1.4535 – 1] = $25,545 × 0.009085 ÷ 0.4535 = $25,545 × 0.02003 = $511 per month

Step 4: Calculate total interest Total paid: $511 × 60 = $30,660 Total interest: $30,660 – $25,545 = $5,115

Making extra payments on a car loan is one of the highest-return financial moves available to most people. Here is what extra payments do to a $25,000 loan at 7% APR on a 60-month term (standard payment: $495/month):

| Extra Monthly Payment | Payoff Time | Interest Saved | Months Saved |

|---|---|---|---|

| $0 (standard) | 60 months | — | — |

| $50 extra | 55 months | $473 | 5 months |

| $100 extra | 51 months | $866 | 9 months |

| $200 extra | 44 months | $1,554 | 16 months |

| $500 extra | 34 months | $2,700 | 26 months |

Even an extra $50 per month saves nearly $500 in interest and pays off the loan 5 months early. Most lenders apply extra payments to the principal by default, but call your lender to confirm — some require you to specify “apply to principal” with each extra payment.

Refinancing your car loan means taking out a new loan at a lower interest rate to pay off your existing loan. It makes sense when:

Refinancing works best when done in the first 1–3 years of a loan, when most of the interest is still in front of you. Refinancing in year 4 of a 5-year loan saves very little because most of the interest has already been paid.

What to watch out for: Some lenders charge prepayment penalties, and rolling too many miles onto an older vehicle can make refinancing impossible (lenders may decline loans on high-mileage vehicles).

Dealers act as middlemen in financing — they connect you with lender partners and are paid a markup on your interest rate. This is called the “dealer reserve” or “finance reserve,” and it can add 1%–2.5% to your APR.

Credit unions consistently offer the most competitive auto loan rates. Unlike banks, credit unions are member-owned and non-profit, meaning they have less incentive to maximize interest income. Membership is often easier to qualify for than people expect — many credit unions accept members who live, work, or worship in a broad geographic area.

The ideal process:

This approach gives you the best of both worlds and prevents the financing conversation from muddying the purchase price negotiation.

An amortization schedule shows every payment over the life of your loan broken down into principal and interest components. It is one of the most useful financial documents most car buyers never look at.

Why it matters:

Our car loan calculator generates a complete, month-by-month amortization schedule for any loan parameters you enter. You can see at a glance how your balance decreases over time, when you will have positive equity, and exactly how much interest you are paying in any given year.

What is a good interest rate for a car loan?

As of 2025–2026, a good interest rate for a new car loan is generally 5%–7% for borrowers with prime credit (660+ score). Below 5% is excellent — typically reserved for borrowers with 720+ scores or manufacturers offering special promotional rates. Above 10% is a signal to either improve your credit before buying or consider a less expensive vehicle.

How much should my car payment be?

Your car loan payment should stay at or below 15% of your monthly take-home pay. If you take home $4,200/month, that is $630/month maximum for the car payment alone, not including insurance and fuel. For a healthier budget, aim for 10%–12%.

Is it better to put more money down or get a shorter loan term?

Both reduce total interest, but they work differently. A larger down payment reduces the loan principal from day one, which helps if you are at risk of being underwater on the loan. A shorter term reduces the number of months you pay interest but requires higher monthly payments. If you have the cash for a larger down payment and can afford higher payments, the combination of both is the best outcome.

Can I pay off a car loan early without penalty?

Most auto loans have no prepayment penalty. Check your loan agreement to confirm. If there is no penalty, paying extra whenever you can is purely beneficial — every dollar of extra principal payment saves you interest for every remaining month of the loan.

Does a car loan hurt your credit?

Initially, yes — a new loan causes a small temporary drop in credit score due to the hard inquiry and new credit account. But a car loan paid consistently and on time is one of the most reliable ways to build credit over 4–5 years. By the time you finish paying, the loan typically has a strongly positive net effect on your credit history.

The single best thing you can do before buying a car is run the numbers yourself — before any dealer sees your credit file or knows your budget. Use our car loan calculator to enter your target vehicle price, expected down payment, your likely interest rate based on your credit score, and your preferred term.

You will know your monthly payment to the dollar, your total interest cost, and your complete amortization schedule. Walk into that dealership knowing every number that matters — and nothing they say will catch you off guard.

[Use the Car Loan Calculator →]