New Car Loan vs. Used Car Loan: Which Is Cheaper? (Full Calculator Comparison)

“Should I buy new or used?” is one of the most common questions in personal finance. Most people try to answer it by comparing the sticker prices. But the real answer requires comparing the total cost of ownership — including your auto loan interest rate, depreciation, insurance, maintenance, and repairs — across the full period you plan to own the vehicle.

This guide puts the new vs. used car loan question through a complete financial analysis, shows you real car loan monthly payment calculations for both scenarios, explains why used car loan rates are always higher than new car rates, and gives you a framework for making the decision that’s genuinely right for your situation.

The Sticker Price Trap — Why Purchase Price Is Only Half the Story

A 3-year-old used car listed at $22,000 looks much cheaper than its new equivalent at $32,000. And in terms of purchase price, it is. But several other factors close that gap significantly:

- Used car loan APRs average 2–5% higher than new car APRs for the same borrower

- New cars come with full manufacturer warranties; used cars may require expensive out-of-pocket repairs

- New cars have lower insurance risk profiles in some categories; older used cars may cost more to insure

- New cars depreciate fastest in year 1–3 (15–25%); a 3-year-old used car has already absorbed that loss

None of this means used is wrong — it often is the smarter choice. But you need to compare the complete picture, not just the purchase price.

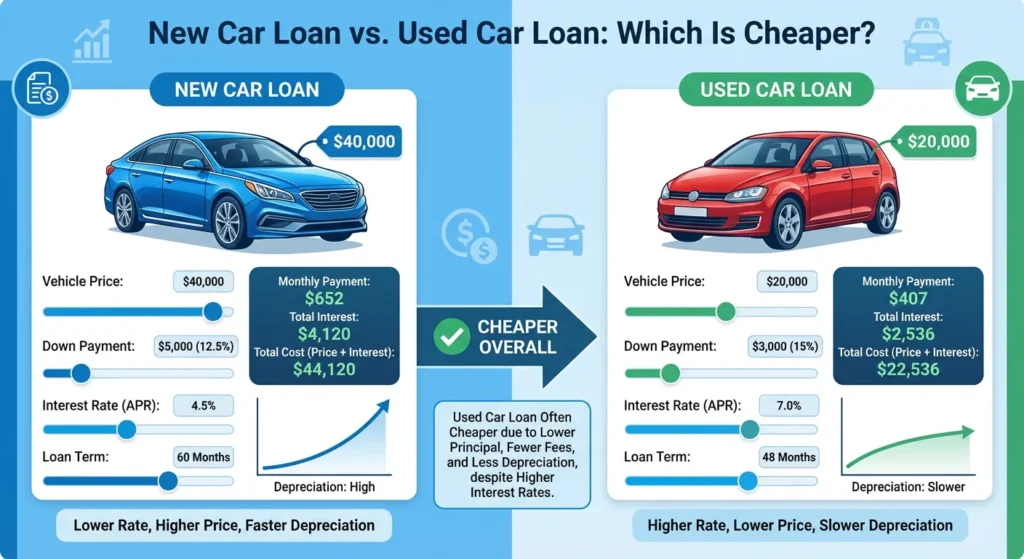

New Car Loan Calculator — Typical 2025 Scenario

2025 Honda CR-V (New):

- MSRP: $34,000

- Down payment: $5,000

- Loan amount: $29,000

- APR (prime borrower): 6.7% (Q1 2025 average per Mercer Capital)

- Loan term: 60 months

- Sales tax (7%): $2,380 (rolled into loan)

- Total financed: $31,380

Monthly payment: $616/month

Total payments: $36,960

Total interest paid: $5,580

Total vehicle cost (including down payment): $41,960

Year 1 depreciation: ~$5,100 (15% on $34,000) Estimated value at loan payoff (60 months): ~$17,000–$19,000

Used Car Loan Calculator — Comparable 2025 Scenario

2022 Honda CR-V (3 years old, ~35,000 miles):

- Sale price: $24,500

- Down payment: $3,000

- Loan amount: $21,500

- APR (prime borrower): 9.5% (used car, Q1 2025 average)

- Loan term: 60 months

- Sales tax (7%): $1,715 (rolled into loan)

- Total financed: $23,215

Monthly payment: $483/month

Total payments: $28,980

Total interest paid: $5,765

Total vehicle cost (including down payment): $31,980

Year 1 depreciation: ~$1,960 (8% on $24,500 — most depreciation already happened) Estimated value at loan payoff (60 months): ~$10,000–$13,000

Side-by-Side Comparison

| Metric | New CR-V | Used CR-V (2022) | Difference |

|---|---|---|---|

| Purchase Price | $34,000 | $24,500 | $9,500 less used |

| APR | 6.7% | 9.5% | 2.8% higher used |

| Monthly Payment | $616 | $483 | $133/mo less used |

| Total Interest | $5,580 | $5,765 | $185 more used |

| Total Cost (5 yr) | $41,960 | $31,980 | $9,980 less used |

| Est. Value at Payoff | $17,500 | $11,500 | $6,000 more new |

| Net Cost (cost − residual) | $24,460 | $20,480 | $3,980 less used |

When you account for residual value (what the car is worth when you pay it off), the used CR-V costs approximately $3,980 less in net terms over 5 years — despite having a higher interest rate. The math favors used in most straightforward comparisons, but the margin is narrower than the sticker price difference suggests.

When the New Car Actually Wins — Specific Scenarios

Manufacturer 0% APR offers. When a manufacturer offers 0% promotional financing, the math can reverse dramatically. On a $32,000 vehicle:

- 0% APR, 60 months: $533/month, $0 interest

- 9.5% APR used car at $24,000: $504/month, $5,765 interest

The new car costs more per month but saves $5,765 in interest. Add reliability and warranty advantages and the new car wins on total value.

When the used car has high mileage or no warranty. A used vehicle with 80,000+ miles and no extended warranty can generate $3,000–$8,000 in repair costs over 5 years. If your used car needs a timing belt, transmission service, or significant mechanical work, the repair costs can easily erase your purchase price savings.

When reliability matters critically. If your livelihood depends on your vehicle — you’re a rideshare driver, a salesperson who travels, or you have no backup transportation — the risk of used car breakdowns carries additional financial weight beyond repair costs.

Interest Rate Reality Check — Why Used Car Rates Are Always Higher

Used car vehicle financing rates are consistently 2–5% higher than new car rates for any given credit tier. There are three structural reasons:

Collateral uncertainty. A used vehicle’s future value is harder to predict. A new car will always be worth approximately 65–75% of purchase price after 3 years and can be quickly sold by the lender if repossessed. A used car with unknown history and undisclosed wear may be worth far less than expected.

Age limitations. Most lenders cap financing on vehicles over 7–10 years old. This restriction itself signals that the collateral becomes riskier with age, and rates increase accordingly.

Borrower pool characteristics. At the market level, used car buyers have slightly lower average credit scores than new car buyers. Lenders price their portfolio risk across the entire borrower pool, which flows through to slightly higher base rates.

Loan Term Differences — New vs. Used

Loan terms available differ between new and used vehicles:

New car loans: Up to 96 months available from most major lenders.

Used car loans: Typically capped at 72 months. For vehicles over 5 years old, many lenders limit terms to 48–60 months. Older vehicles (8+ years) may only qualify for 36–48 month terms.

This matters for your auto loan payment estimator calculations. A used car with a shorter maximum available term may have a higher monthly payment than the sticker price difference would suggest.

The Down Payment Question — New vs. Used

Financial experts recommend different down payment targets depending on vehicle type:

New car: 20% down minimum. New cars depreciate fastest in year one — sometimes 15–20% in the first 12 months. A 20% down payment ensures you’re not immediately underwater on your loan.

Used car: 10% down minimum. Most of the depreciation has already occurred, reducing your negative equity risk. However, a larger down payment still reduces your interest costs and monthly payment.

Use the car loan down payment calculator to see exactly how different down amounts change your monthly payment and total interest. The visual slider makes it immediately clear that every additional $1,000 down saves real money.

Certified Pre-Owned (CPO) — The Middle Ground

Certified Pre-Owned vehicles offer a compromise between new and used:

- Price: 15–30% less than new equivalent

- Rate: Often close to new car rates through manufacturer captive finance (Toyota Financial, Ford Credit, etc.)

- Warranty: Full manufacturer-backed warranty (often 2–3 additional years)

- Condition: Inspected and certified to manufacturer standards

A CPO vehicle at $28,000 with a 7.0% APR (vs. 9.5% for a non-CPO used car) offers better pricing than new with better rates and protection than a standard used vehicle. It’s frequently the best value in the market for buyers who want reliability without full new-car depreciation.

How the Used Car Market Has Changed in 2025

In Q1 2025, the average amount financed for new vehicles rose to $41,720, up modestly from $40,610 in Q1 2024, while the average interest rate held steady at 6.7% annually with monthly payments averaging $745 for new loans. In the used vehicle segment, monthly payments remained largely flat at $521 per month with an average term of 67.2 months, and the average interest rate held steady at 11.9%.

These numbers reveal an important reality: the average car buyer is financing over $40,000 for new vehicles — a figure that makes down payment, rate negotiation, and term selection more impactful than ever.

The average auto loan delinquency rate shows that used vehicle delinquencies are higher than new vehicle delinquencies, reflecting the different risk profiles of borrowers in each segment.

New vs. Used Decision Framework

Use this checklist to guide your decision:

Choose New if:

- ✅ A 0% or sub-5% promotional APR is available

- ✅ You plan to keep the vehicle 7+ years

- ✅ You drive high mileage annually (new cars handle it better)

- ✅ Reliability is critical and you have no repair fund

- ✅ You want the latest safety technology

- ✅ You can put 20% down to offset first-year depreciation

Choose Used if:

- ✅ The used car is 2–4 years old (sweet spot: depreciation done, mechanically sound)

- ✅ You have good credit to minimize the rate penalty

- ✅ You’re buying a CPO vehicle with manufacturer backing

- ✅ Total ownership cost over 5 years clearly favors used in your calculations

- ✅ Your monthly budget is constrained and the lower payment matters

Run the Numbers: Put both scenarios into a vehicle loan calculator with the actual prices, your expected APR, and the same loan term. Compare total 5-year cost, not just monthly payment or purchase price.

Leasing vs. Buying — Brief Overview

Leasing is a third option that’s often misunderstood. A lease is not a loan — you’re paying for the vehicle’s depreciation during your lease term, not building equity. Leasing makes sense if:

- You want a new car every 2–3 years

- You drive under 12,000–15,000 miles/year

- You don’t want to deal with major repairs

- Lower monthly payments are a priority over ownership

Leasing has gained traction, rising to 24.7% of new vehicle transactions in Q1 2025, up from 23.7% during Q1 2024 and 19.2% in Q1 2023.

However, leasing generates no equity. After 36 months of payments, you return the car with nothing to show for it. Over a 10-year horizon, ownership — whether new or used — almost always generates more value than perpetual leasing.

Full Cost Comparison: New vs. Used vs. Lease Over 10 Years

Assuming you get a new/used car every 5 years (one transaction cycle):

| Strategy | 10-Year Total Cost | Notes |

|---|---|---|

| New car, 5yr loan, sell after 5 yrs | ~$49,000 | After selling for $17K |

| Used car (3yr old), 5yr loan, sell after 5 yrs | ~$36,000 | After selling for $8K |

| New car, lease twice (2×3yr) | ~$43,000 | No equity built either time |

| CPO vehicle, 5yr loan, sell after 5 yrs | ~$40,000 | Best blend of cost and reliability |

These numbers use the CR-V scenario above and are illustrative. Your actual results depend on specific vehicles, care, mileage, and market conditions. The point is that used CPO vehicles consistently generate the best 10-year total cost for the majority of buyers who don’t drive extreme mileage.

Try our Auto Loan Calculator to run your specific new vs. used comparison with real numbers.