How to Calculate Auto Loan Interest: Complete Formula, Examples & Money-Saving Strategies

If you’ve ever stared at a car loan offer wondering exactly how much you’re really paying for the privilege of borrowing money, you’re not alone. Most car buyers focus entirely on the monthly payment number — but the true cost of auto loan interest is often two, three, or even four times higher than people expect. By the time you make your final payment on a 72-month loan, you may have paid thousands of dollars in interest that never went toward owning your vehicle.

This guide breaks down exactly how auto loan interest is calculated, walks through real-world examples using the standard car loan interest formula, and shows you every legitimate strategy to reduce what you pay. Whether you’re financing a new car, shopping for a used car loan, or thinking about refinancing, understanding the math behind your loan puts you in control.

What Is Auto Loan Interest and How Does It Work?

When a lender gives you money to buy a vehicle, they charge you a fee for that service. That fee is interest — expressed as an annual percentage rate, or APR. Your APR is applied to your outstanding loan balance every single month. As your balance decreases with each payment, the dollar amount of interest charged also decreases. This system is called amortization, and it’s how virtually every vehicle loan EMI in the United States is structured.

The critical thing to understand about amortizing loans is that your lender front-loads the interest. In the early months of your loan, the majority of each payment goes toward interest rather than principal. In the final months, it flips — most of your payment is reducing your actual balance. This is why paying off a loan early or making extra payments is so financially powerful.

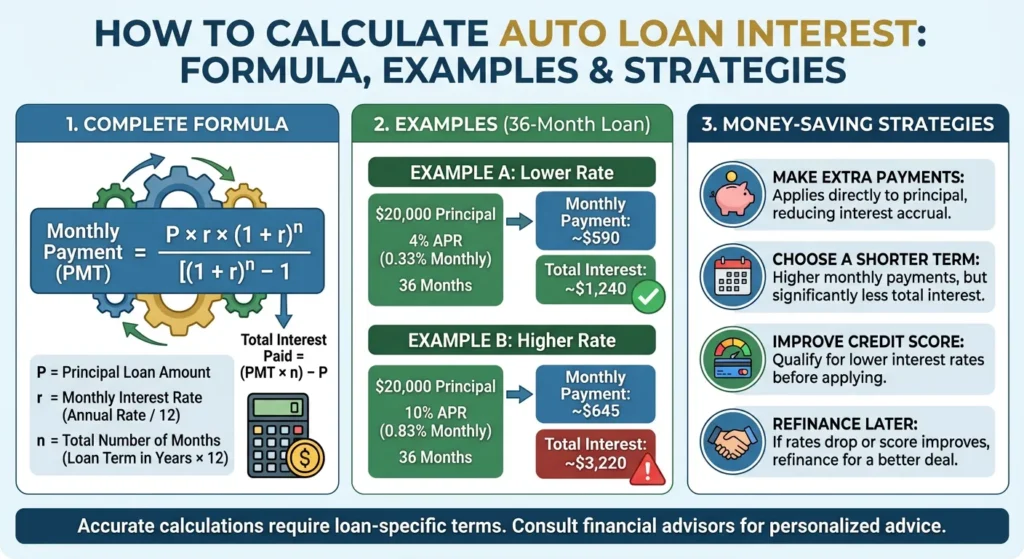

The Car Loan Interest Formula — Step by Step

Every bank, credit union, and dealership uses the same mathematical formula to calculate your monthly car payment. It’s called the standard loan amortization formula:

Monthly Payment (M) = P × [r(1+r)ⁿ] ÷ [(1+r)ⁿ − 1]

P = Principal (amount borrowed)

r = Monthly interest rate (Annual APR ÷ 12 ÷ 100)

n = Total number of payments (loan term in months)

This is the core car loan interest formula that drives every auto loan calculator, every bank’s system, and every dealer’s finance office software. Let’s apply it to a real example.

Auto Loan Interest Calculation — Worked Example

Scenario:

- Vehicle price: $28,000

- Down payment: $3,000

- Loan principal (P): $25,000

- Annual APR: 7.5%

- Loan term: 60 months

Step 1: Convert APR to monthly rate r = 7.5% ÷ 12 ÷ 100 = 0.00625

Step 2: Calculate (1 + r)ⁿ (1.00625)⁶⁰ = 1.4536

Step 3: Apply the formula M = 25,000 × [0.00625 × 1.4536] ÷ [1.4536 − 1] M = 25,000 × 0.009085 ÷ 0.4536 M = 25,000 × 0.020024 M ≈ $500.60 per month

Step 4: Calculate total interest paid Total payments = $500.60 × 60 = $30,036 Total interest = $30,036 − $25,000 = $5,036

That means for a $25,000 loan at 7.5% APR over 5 years, you’ll pay over $5,000 purely in interest — money that goes to the lender and builds zero equity in your vehicle. This is why using an auto loan interest calculator before you sign any paperwork is so important.

How Amortization Splits Your Monthly Payment

Here’s a look at how the first and last several payments break down on this $25,000 loan:

| Payment # | Monthly Payment | Principal Paid | Interest Paid | Remaining Balance |

|---|---|---|---|---|

| 1 | $500.60 | $344.35 | $156.25 | $24,655.65 |

| 6 | $500.60 | $352.55 | $148.05 | $23,372.02 |

| 12 | $500.60 | $362.13 | $138.47 | $21,924.15 |

| 24 | $500.60 | $381.97 | $118.63 | $18,931.80 |

| 36 | $500.60 | $403.34 | $97.26 | $15,734.48 |

| 48 | $500.60 | $425.69 | $74.91 | $12,362.38 |

| 60 | $500.60 | $497.99 | $3.11 | $0.00 |

Notice how payment #1 sends $156 to interest but only $344 toward principal. By payment #48, that balance flips dramatically — $425 is reducing your loan balance while only $75 goes to interest. This progression is at the heart of auto loan principal and interest dynamics, and it’s exactly why making extra payments early in your loan has the biggest possible impact.

The Real Cost of Different Interest Rates — Side by Side

Using the same $25,000 loan over 60 months, here’s how different APRs change your cost:

| APR | Monthly Payment | Total Interest | Total Paid |

|---|---|---|---|

| 4.0% | $460.41 | $2,624.60 | $27,624.60 |

| 5.5% | $479.02 | $3,741.20 | $28,741.20 |

| 7.5% | $500.60 | $5,036.00 | $30,036.00 |

| 10.0% | $531.18 | $6,870.80 | $31,870.80 |

| 14.0% | $581.32 | $9,879.20 | $34,879.20 |

| 18.0% | $635.45 | $13,127.00 | $38,127.00 |

The difference between a 4% APR and an 18% APR on this single loan is $10,502 in extra interest. That’s not a rounding error — it’s the cost of a solid used car. This is the single most powerful argument for improving your credit score before applying for auto financing.

6 Proven Strategies to Reduce Your Auto Loan Interest

1. Improve Your Credit Score Before Applying

Your credit score is the single biggest lever on your auto loan interest rate. Moving from a 620 (subprime) to a 720 (prime) score can cut your APR by 4–7 percentage points, saving thousands over the life of any vehicle loan. Even 90 days of focused credit improvement — paying down credit card balances, disputing errors, avoiding new accounts — can meaningfully move your score.

2. Make a Larger Down Payment

Your down payment directly reduces your principal, which reduces both your monthly vehicle loan EMI and your total interest. Every additional $1,000 down eliminates approximately $100–$150 in total interest on a 60-month loan at 7% APR.

3. Choose the Shortest Loan Term You Can Comfortably Afford

The auto loan term is the second most important factor in total interest paid. A 36-month loan on $25,000 at 7% APR costs $2,783 in total interest. The same loan over 72 months costs $5,716 — more than double. Shorter terms mean higher monthly payments but dramatically lower total costs.

4. Shop for the Best Auto Loan Rates Before Visiting a Dealer

Get pre-approved by your bank and credit union before walking into any dealership. Having a pre-approval letter in hand gives you a concrete benchmark to compare dealer financing against. Credit unions consistently offer the best auto loan rates available, often 0.5–2% lower than commercial banks for equivalent credit profiles.

5. Make Extra Monthly Payments — Any Amount Helps

Extra payments reduce your principal balance faster, which reduces future interest charges because interest is always calculated on the remaining balance. Even an extra $50/month on a $25,000 loan at 7% APR saves approximately $320 in interest and pays off the loan 4 months early. Use an auto loan payoff calculator to see the exact impact of any extra payment amount.

6. Refinance When Rates Drop or Your Credit Improves

If you took out your loan when rates were high or your credit was poor, refinancing can generate significant savings. A borrower who took a $25,000 loan at 11% in 2023 and refinances to 7% in 2025 with 40 months remaining saves approximately $2,100 in remaining interest payments.

Common Mistakes That Cost You Extra Interest

Focusing only on the monthly payment. Dealers know that buyers respond to low monthly numbers. They’ll stretch your loan to 84 months to get the payment down, even though this costs you thousands extra. Always calculate total interest, not just the EMI.

Not accounting for fees in your loan amount. Rolling documentation fees, extended warranties, and GAP insurance into your loan increases your principal — and therefore your total interest. Every $1,000 added to the principal adds approximately $100–$180 in extra interest over a 60-month term.

Skipping the amortization schedule. Understanding the full loan amortization calculator output tells you exactly when you’ll break even on a refinance, how much equity you have at any point, and the best time to make a lump-sum extra payment.

Accepting the first financing offer. Studies consistently show that borrowers who shop around save an average of $1,000–$1,500 over the life of their loan. Getting three quotes takes less than an hour and can be done entirely online.

Use an Auto Loan Calculator to Run Every Scenario

The formulas above are accurate, but doing the math manually for every scenario is tedious. A free auto loan interest calculator lets you instantly compare:

- How changing the APR by 1% affects your total cost

- What adding $100/month extra would save in interest

- Whether a shorter term with higher payments actually saves money

- How much total interest you’ll pay at the lender’s offered rate vs. your credit union’s rate

Run every major decision through a car loan interest calculator before signing. Five minutes of calculation can save you thousands of dollars over the life of your loan.

Key Takeaways

- Auto loan interest is calculated monthly on your remaining balance using the amortization formula

- Early payments are mostly interest; later payments are mostly principal

- The difference between 4% and 18% APR on a $25,000 loan is over $10,000 in extra interest

- Your credit score, loan term, and down payment are the three biggest levers on your total interest cost

- Extra payments made early in the loan have the greatest impact on interest savings

- Always compare total cost of the loan — not just monthly payment — when evaluating offers

Use our free Auto Loan Calculator to run these calculations instantly with your own numbers.