Car Loan Amortization Schedule Explained: How to Read It, Use It & Pay Off Your Loan Early

Most people who take out an auto loan never look at their amortization schedule. This is a financially costly mistake. Your loan amortization calculator output — a complete month-by-month breakdown of every payment for the life of your loan — contains information that can save you hundreds or thousands of dollars if you know how to read it and act on it.

This guide explains exactly what an amortization schedule shows, why the numbers look the way they do, how to use the schedule to make smarter payment decisions, and what the math tells you about every early payoff strategy available to car buyers.

What Is a Loan Amortization Schedule?

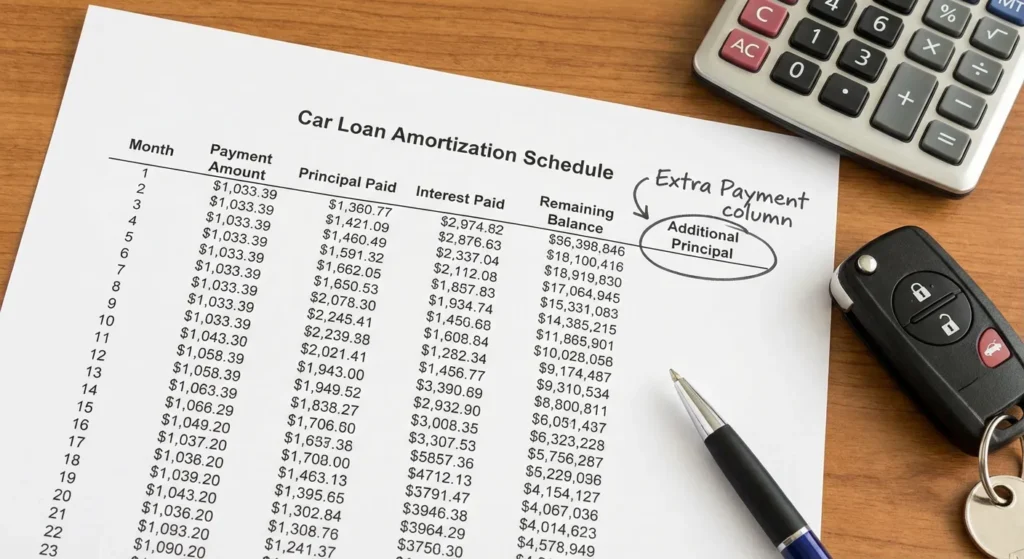

An amortization schedule is a complete table showing every payment you’ll make over your loan term. For each payment, it shows:

- Payment number and date — Which payment this is and when it’s due

- Total payment amount — Your fixed monthly car payment (EMI)

- Principal portion — How much of this payment reduces your actual loan balance

- Interest portion — How much of this payment goes to the lender as their fee

- Remaining balance — What you still owe after this payment

- Cumulative interest — Total interest paid from your first payment to this one

These six columns tell you everything about your loan’s financial progress. Every single car finance calculator that generates a full schedule is showing you this exact data — but most car buyers only look at the monthly payment number and ignore the rest.

The Core Insight: Why Early Payments Are Mostly Interest

Here’s the number that surprises almost everyone who sees their amortization schedule for the first time:

On a $25,000 loan at 7.5% APR over 60 months:

- Payment #1: $156 interest, $344 principal (31% of payment is pure interest)

- Payment #6: $148 interest, $352 principal

- Payment #12: $138 interest, $362 principal

- Payment #24: $119 interest, $382 principal

- Payment #36: $97 interest, $404 principal

- Payment #48: $75 interest, $426 principal

- Payment #60: $3 interest, $498 principal

Your first 12 payments send over $1,600 to interest alone — that’s $1,600 in real money that purchased zero car, built zero equity, and will never be recovered. By the time you hit the halfway point (month 30), you’ve paid approximately 55% of your total interest but have only reduced your balance by about 43%.

This front-loading of interest is a mathematical inevitability of amortization — it’s not a predatory trick. But understanding it explains why:

- Making extra payments early in the loan saves far more than making them late

- Refinancing in the first half of a loan generates much better savings than refinancing later

- Down payments have a significant multiplier effect on total interest savings

Reading a Real Amortization Schedule — Full Example

Loan: $20,000 at 6.5% APR, 48 months Monthly payment: $476.27

| Month | Payment | Principal | Interest | Balance | Cumul. Interest |

|---|---|---|---|---|---|

| 1 | $476.27 | $368.94 | $108.33 | $19,631.06 | $108.33 |

| 3 | $476.27 | $370.94 | $105.33 | $18,887.24 | $320.67 |

| 6 | $476.27 | $375.00 | $101.27 | $17,768.83 | $642.82 |

| 12 | $476.27 | $383.20 | $93.07 | $15,497.58 | $1,268.92 |

| 18 | $476.27 | $391.57 | $84.70 | $13,182.74 | $1,856.40 |

| 24 | $476.27 | $400.11 | $76.16 | $10,821.79 | $2,406.44 |

| 30 | $476.27 | $408.83 | $67.44 | $8,412.63 | $2,918.12 |

| 36 | $476.27 | $417.74 | $58.53 | $5,953.40 | $3,390.22 |

| 42 | $476.27 | $426.84 | $49.43 | $3,442.30 | $3,822.42 |

| 48 | $476.27 | $432.77 | $2.34 | $0.00 | $4,060.96 |

Total interest paid: $4,060.96

By month 12 (25% of the loan term), you’ve paid $1,269 in interest but your balance has only dropped by $4,502 — from $20,000 to $15,498. You’ve made 12 payments totaling $5,715, but only $4,502 of that went toward owning your car.

Yearly Amortization View — The Big Picture

For a longer loan (60 months, $25,000 at 7.0%), the yearly view reveals how the interest cost is distributed across the loan’s life:

| Year | Payments Made | Total Paid | Principal Paid | Interest Paid | Balance at Year End |

|---|---|---|---|---|---|

| Year 1 | 12 | $5,944 | $4,218 | $1,726 | $20,782 |

| Year 2 | 12 | $5,944 | $4,522 | $1,422 | $16,260 |

| Year 3 | 12 | $5,944 | $4,847 | $1,097 | $11,413 |

| Year 4 | 12 | $5,944 | $5,196 | $748 | $6,217 |

| Year 5 | 12 | $5,944 | $5,561 | $383 | $0 |

| Total | 60 | $29,720 | $25,000 | $4,720 |

Year 1 interest ($1,726) is 4.5x higher than Year 5 interest ($383). This decay is the financial foundation of every early payoff strategy that actually works.

How Extra Monthly Payments Change Your Amortization

This is where reading your amortization schedule gets genuinely exciting. Extra payments don’t just help — they have a compounding benefit because every dollar that reduces your principal today eliminates all future interest that would have been charged on that dollar.

Same $25,000 loan at 7.0% APR, 60 months — with extra payments:

| Extra Monthly | Months to Payoff | Total Interest | Interest Saved | Months Saved |

|---|---|---|---|---|

| $0 | 60 | $4,720 | — | — |

| $50 | 56 | $4,394 | $326 | 4 months |

| $100 | 52 | $4,094 | $626 | 8 months |

| $150 | 49 | $3,818 | $902 | 11 months |

| $200 | 46 | $3,562 | $1,158 | 14 months |

| $300 | 41 | $3,095 | $1,625 | 19 months |

| $500 | 35 | $2,303 | $2,417 | 25 months |

An extra $200/month doesn’t just save the $200 × months saved in payments — it saves $1,158 in total interest and gets you debt-free 14 months earlier. The auto loan payoff calculator in Tab 3 shows this exact calculation for any extra payment amount you enter.

Lump-Sum Extra Payments — When Are They Most Effective?

A lump-sum payment (like a tax refund or bonus) applied directly to your auto loan balance generates maximum savings when applied as early in the loan as possible. Here’s why:

On a $25,000 loan at 7.0% APR with 60 months remaining, a $2,000 lump-sum payment applied at:

| Timing | Interest Saved | Months Saved |

|---|---|---|

| Month 1 | $820 | 4.8 months |

| Month 12 | $680 | 4.0 months |

| Month 24 | $530 | 3.1 months |

| Month 36 | $360 | 2.1 months |

| Month 48 | $155 | 0.9 months |

The same $2,000 saves 5.3x more interest if applied in Month 1 vs. Month 48. This is why financial advisors emphasize making extra payments early in the loan, not waiting until you have a large amount saved.

Using Your Amortization Schedule to Track Equity

Your amortization schedule tells you exactly how much equity you have in your vehicle at any point in time. To calculate your equity:

Vehicle Equity = Current Market Value − Remaining Loan Balance

Use your amortization schedule to find your balance at any given month, then compare it to the vehicle’s current market value on Kelley Blue Book or Edmunds.

Example at Month 18 of a 60-month, $25,000 loan at 7.0%:

- Remaining balance per schedule: ~$17,300

- Vehicle market value (assuming $28,000 purchase, 3yr-old CRV model): ~$20,500

- Your equity: ~$3,200

Positive equity means you could sell the car, pay off the loan, and pocket the difference. Negative equity (being “underwater” or “upside-down”) means the vehicle is worth less than your balance — common in early months of long-term loans.

Negative Equity — How It Shows Up in Your Amortization

On a 72-month loan at 9.0% APR for a $32,000 vehicle (no down payment):

| Month | Loan Balance | Estimated Car Value | Equity |

|---|---|---|---|

| 0 | $32,000 | $32,000 | $0 |

| 6 | $29,600 | $26,240 | -$3,360 |

| 12 | $27,100 | $22,400 | -$4,700 |

| 24 | $21,700 | $17,920 | -$3,780 |

| 36 | $15,800 | $14,720 | -$1,080 |

| 48 | $9,500 | $12,160 | +$2,660 |

| 60 | $2,900 | $10,240 | +$7,340 |

| 72 | $0 | $8,960 | +$8,960 |

Notice how the borrower is underwater from Month 6 through Month 42 — a period of nearly 3 years. During this window, if you need to sell, trade in, or if the car is totaled, you owe more than the vehicle is worth. This is why GAP insurance is recommended for borrowers with long loan terms and minimal down payments.

Amortization Schedule vs. Simple Interest — Key Difference

All standard car loans in the United States use pre-computed amortization — meaning your payment schedule is calculated at origination and fixed for the life of the loan. Some older or specialized loans use simple interest calculations where interest accrues daily on your outstanding balance.

For simple interest loans, paying early (even by a few days) reduces the interest charged on that payment. For pre-computed amortization loans (which most car loans are), the total interest is already determined by the loan terms — though extra principal payments still reduce future interest charges.

How to Use the Amortization Tab in the Auto Loan Calculator

Our loan amortization calculator in Tab 3 builds your complete schedule automatically. Here’s how to use it effectively:

Step 1: Complete your loan inputs in Tab 1 first — Vehicle price, down payment, APR, term, start date. The amortization schedule pulls from these values.

Step 2: Add an extra monthly payment (optional) — Enter any extra monthly amount in the Calculator tab. The amortization schedule and payoff summary cards update to reflect your accelerated schedule.

Step 3: Toggle Monthly vs. Yearly view — Monthly view shows every individual payment (best for tracking your exact balance). Yearly view aggregates by year (best for big-picture planning).

Step 4: Read the Payoff Summary Cards — At the top of Tab 3, three cards show:

- Scheduled payoff date (no extra payments)

- Early payoff date (with your extra payment)

- Total interest saved

Step 5: Find your balance at any specific date — Scroll to the payment row corresponding to any future date to see exactly what your balance will be. This is useful for planning a refinance, calculating equity, or deciding when to sell.

Step 6: Look at cumulative interest — The final column shows total interest paid to date. If you’re considering paying off the loan at a specific month, this tells you exactly how much the loan has cost you in interest so far.

The Payoff Crossover Point — Your Most Important Number

Every amortizing loan has a “crossover point” — the specific payment where more of your monthly payment is going to principal than to interest. For most loans, this happens somewhere around the halfway mark.

For a $25,000 loan at 7.0% APR over 60 months:

- Payment #1: 71% principal, 29% interest

- Payment #30: 83% principal, 17% interest

- Payment #60: 99.4% principal, 0.6% interest

For a longer term loan (72 months at 8.5% APR):

- Payment #1: 66% principal, 34% interest

- Payment #36: 72% principal, 28% interest

- Payment #72: 99.6% principal, 0.4% interest

The crossover happens later on longer-term, higher-rate loans — meaning a greater proportion of your early payments is consumed by interest. This is the mathematical argument against 72–84 month auto loan terms for most buyers.

Three Amortization-Based Strategies That Save Real Money

Strategy 1: The “Bi-Weekly Payment” Method

Instead of making one monthly payment, make half your monthly payment every two weeks. Because there are 52 weeks in a year, this results in 26 half-payments = 13 full payments per year instead of 12.

Effect on a $25,000 loan at 7.0% APR, 60 months:

- Standard 12 payments/year: Payoff in 60 months, $4,720 total interest

- Bi-weekly payments: Payoff in ~56 months, ~$4,376 total interest

- Savings: $344 and 4 months — at zero extra cost, just by changing payment timing

Many lenders allow bi-weekly payments. Alternatively, simply add 1/12 of your monthly payment to each monthly payment (the mathematical equivalent).

Strategy 2: The “Annual Tax Refund” Method

Apply your entire federal tax refund directly to your auto loan principal in Month 1–12 of your loan. The average U.S. refund in 2024 was approximately $3,100.

Effect of $3,100 applied in Month 3 of $25,000 loan at 7.0%, 60 months:

- Without lump sum: 60 months, $4,720 total interest

- With $3,100 in Month 3: ~51 months, ~$3,510 total interest

- Savings: $1,210 and 9 months

Strategy 3: The “Pay Previous Payment” Method

When you refinance to a lower rate (resulting in a lower monthly payment), keep paying your original, higher payment amount. The difference goes straight to principal.

Example: Original payment $600, refinance reduces to $520. Keep paying $600. The extra $80/month accelerates your payoff and eliminates additional interest above and beyond the rate savings from refinancing.

Amortization Quick Reference: How Much Extra Per Month to Pay Off in X Years

If your loan’s scheduled term is 60 months and you want to pay it off in fewer years:

| Loan Amount | Original APR | Pay Off in 4 Years | Pay Off in 3 Years |

|---|---|---|---|

| $20,000 | 7.0% | +$90/mo | +$225/mo |

| $25,000 | 7.0% | +$113/mo | +$283/mo |

| $30,000 | 7.0% | +$135/mo | +$338/mo |

| $35,000 | 8.0% | +$175/mo | +$420/mo |

Use the auto loan payoff calculator to find the exact extra payment needed for your specific loan and desired payoff date.