11

11

Right now, approximately 900,000 borrowers with credit scores between 720 and 759 are paying 9–11% APR on their auto loans — rates they could reduce by refinancing. According to Equifax’s 2025 Market Pulse data, 60% of borrowers with a VantageScore above 680 and high APRs are ready to refinance and are twice as likely to take action. If you’re one of them, the question isn’t whether refinancing saves money — it almost certainly does. The question is how much, and whether the timing is right.

This comprehensive guide explains exactly how the refinance auto loan calculator process works, when it makes financial sense, where to find the best refinance rates, and how to execute the refinance from application to final approval.

Refinancing your car loan means taking out a new loan to pay off your existing one. Your new lender pays your old lender directly, and you begin making payments to the new lender at the new (hopefully lower) rate. The vehicle remains yours throughout the process — refinancing doesn’t affect your title or registration.

You can refinance to achieve three different goals:

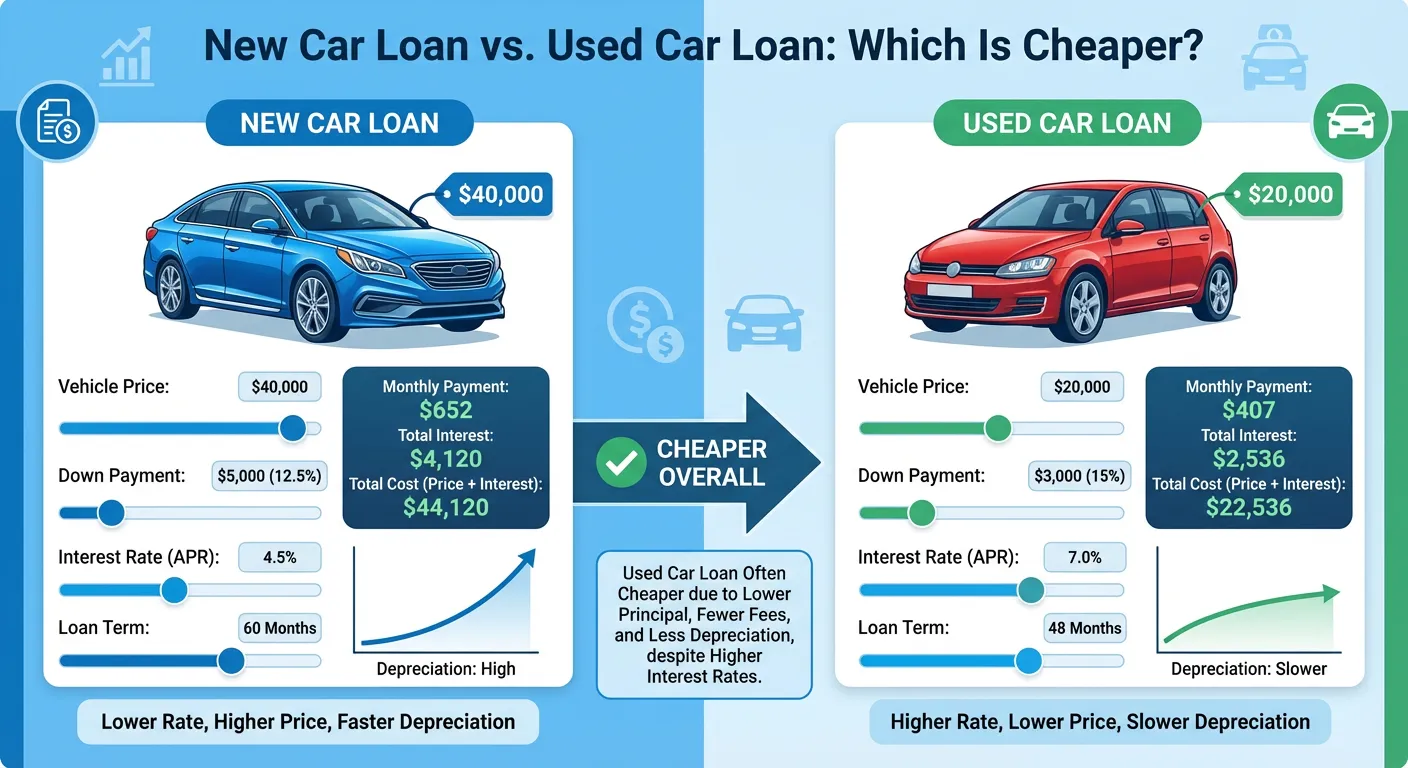

Lower your interest rate — The most common reason. If your credit score has improved since your original loan or market rates have fallen, refinancing to a lower APR reduces your total interest cost.

Lower your monthly payment — By extending your loan term during refinancing, you spread payments over more months, reducing your monthly obligation. Important caveat: this increases your total interest paid.

Shorten your loan term — By refinancing to a shorter term (with potentially the same or lower rate), you pay off the loan faster and reduce total interest — though your monthly payment increases.

Original loan (taken when credit was 620):

Refinance offer (credit score now 720):

Result:

For 15 minutes of paperwork, that’s an extraordinary return.

Original loan (taken in 2023 at peak rates):

Refinance offer (rates fallen in 2025):

Result:

Modest but real — over $1,000 saved with minimal effort.

Original loan:

Refinance: extend to 60 months at same rate:

Result:

This scenario trades higher long-term cost for short-term cash flow relief. It’s a legitimate strategy if you need to free up monthly budget, but understand you’re paying for that convenience with extra interest.

Use a refinance auto loan calculator to confirm the numbers before applying, but refinancing generally makes sense when:

The most impactful reason to refinance. If your score has risen 50+ points since your original loan, you likely qualify for a meaningfully lower APR. Even a 3–4 point improvement in rate on a $20,000 balance saves $1,000–$2,000 in total interest.

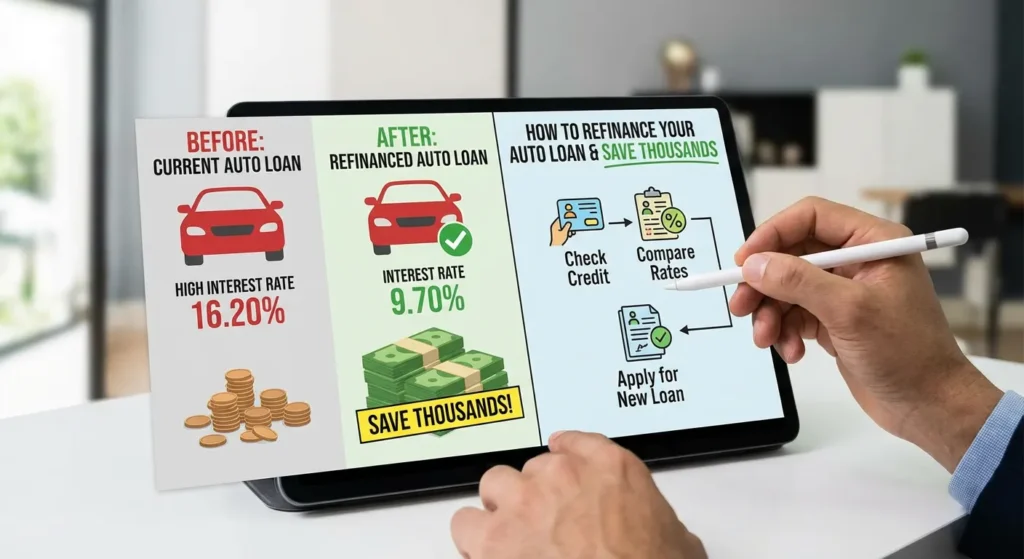

After the Federal Reserve began cutting rates in September 2024 (three consecutive cuts through December), many borrowers who took loans in 2022–2023 at peak rates can now refinance at meaningfully lower APRs. If your rate is above 9% on a new car or above 12% on a used car, check current offerings.

Dealers legally mark up the wholesale rate they receive from lenders by 1–3% as profit (called “dealer reserve”). If you accepted dealer financing without comparing outside offers, you’re likely paying 1–2% more than necessary. Refinancing at your bank or credit union rate recovers that spread immediately.

Refinancing is most valuable early in your loan because you have the most interest-bearing balance remaining. If you’re in the final 12–18 months of a 60-month loan, most of your interest is already paid and refinancing generates minimal savings.

“Significantly” means at least 1.5–2 percentage points lower. Small differences (0.25–0.5%) may not justify the minor credit impact and administrative effort of refinancing.

Some lenders (particularly in subprime auto lending) include prepayment penalties — fees for paying off your loan early. Check your current loan agreement. If a penalty exists, calculate whether the interest savings exceed the penalty cost.

By the midpoint of any amortizing loan, most of the interest has already been paid. Refinancing the remaining balance generates minimal savings even at a lower rate.

Some refinance lenders charge origination fees or title transfer fees. On a small remaining balance, these fees may offset the interest savings entirely.

If your credit has worsened since your original loan, refinancing will likely result in a higher rate offer, not lower. There’s no value in refinancing into a worse rate.

Most lenders won’t refinance vehicles over 7–10 years old or with more than 100,000–125,000 miles. Check eligibility criteria before applying.

Before applying anywhere, pull your current loan statement and record:

Pull your free credit report at AnnualCreditReport.com. Your FICO score determines what rates you’ll be offered. If your score is below 650, consider whether 60–90 days of credit building before applying could get you a materially better rate.

Lenders need the vehicle’s:

Lenders typically won’t refinance if the vehicle’s value is significantly lower than the outstanding balance (high LTV).

Apply to 3–5 lenders within a 14–45 day window. All applications in this window count as a single hard inquiry for FICO scoring purposes, so there’s no penalty for shopping around. Apply to:

Don’t just compare monthly payments — compare total interest paid over the new term. Use the car loan comparison calculator to enter your current payoff amount and remaining months (Loan A) vs. each refinance offer (Loan B). The tool shows you exactly how much each option costs in total.

If the refinance has any fees, calculate how many months it takes to recover them through monthly savings:

Break-Even Months = Total Fees ÷ Monthly Payment Savings

Example: $300 in fees ÷ $65/month savings = 4.6 months to break even

If you plan to keep the loan longer than the break-even point, refinancing is profitable.

Once you’ve chosen the best offer:

Still the top option. Most credit unions have simple online refinance applications and fast approvals. Rates typically run 0.5–2% below commercial banks.

One of the largest and most accessible online auto refinance lenders. Pre-qualification available with no credit impact. Good for borrowers with 620+ scores.

Best for borrowers with excellent credit (720+). Offers some of the lowest auto refinance rates available, no fees, and same-day funding in many cases.

Competitive rates for existing customers. Worth checking as part of your comparison if you already bank there.

These are refinance-focused marketplaces that submit your application to multiple lenders simultaneously. Useful if you want to minimize the number of individual applications you manage.

Refinancing has a minor, temporary effect on your credit:

Hard inquiry: Each lender you apply to performs a hard credit pull, which reduces your score by 2–5 points. Multiple inquiries within 14–45 days count as one inquiry for auto loan purposes under FICO scoring.

Account opening: Your new loan appears as a new account, slightly reducing your average account age — a minor negative.

Account closure: Your old loan is paid off and closed, which can affect your credit mix slightly.

Net impact: Most borrowers see a temporary dip of 5–15 points, fully recovering within 3–6 months of on-time payments on the new loan. The long-term credit effect of successfully managing a refinanced loan is positive.

Use this table to estimate your savings before using the full calculator:

Monthly Payment Reduction by Rate Decrease (Per $10,000 Balance, 36 Months Remaining):

| Rate Reduction | Monthly Savings | Total Savings |

|---|---|---|

| 1.0% lower | ~$5/month | ~$180 |

| 2.0% lower | ~$9/month | ~$324 |

| 3.0% lower | ~$14/month | ~$504 |

| 4.0% lower | ~$18/month | ~$648 |

| 5.0% lower | ~$23/month | ~$828 |

For larger balances and longer remaining terms, multiply proportionally. A $25,000 balance with 48 months remaining and a 4% rate reduction saves approximately $1,620 in total interest.

Set up autopay. Many lenders offer a 0.25% APR discount for autopay enrollment. On a $20,000 balance, that saves approximately $150 in total interest.

Keep making your old payment amount. If your refinance reduced your monthly payment by $70, keep paying the old amount. That extra $70/month goes directly to principal, accelerating your auto loan payoff and saving additional interest.

Track your payoff date. Use the amortization schedule feature of an auto loan calculator to see exactly when you’ll own the vehicle free and clear under your new terms.

Use our free Auto Loan Refinance Calculator to see exactly how much you’d save by refinancing today.